DIFC vs ADGM: The UAE’s Financial and Tech Power Struggle and What It Means for Business and Real Estate

The United Arab Emirates is in the middle of a defining economic shift. Finance, artificial intelligence, technology, and global capital flows are converging at speed, and the country’s ambition is no longer regional leadership alone, but genuine global relevance. At the centre of this transformation sit two powerful financial free zones: Dubai International Financial Centre and Abu Dhabi Global Market.

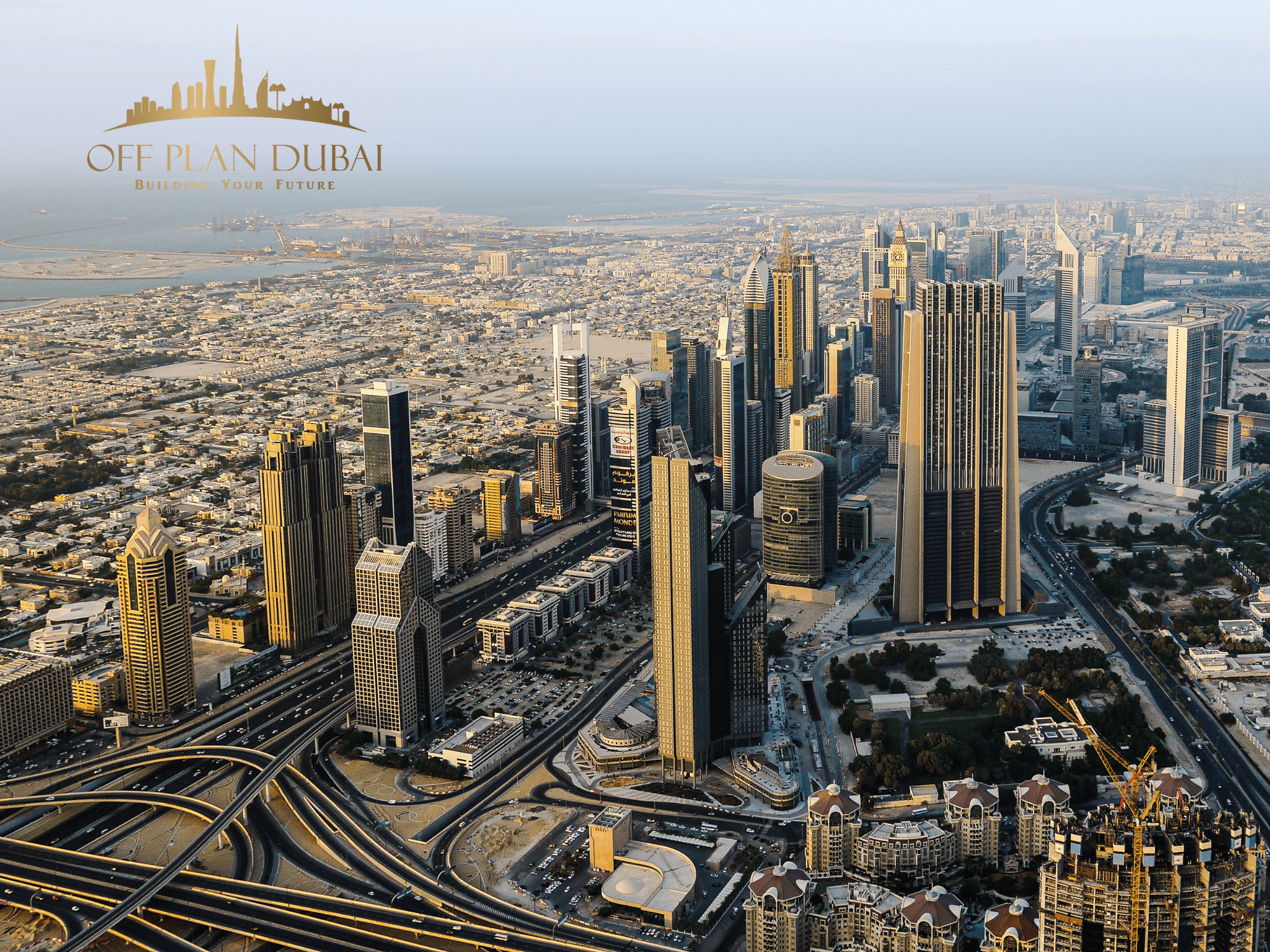

Dubai’s recent announcement of a major extension to DIFC, with a second phase estimated to exceed one hundred billion dollars in total investment value, has reignited debate about where the true centre of gravity for finance, AI and technology in the UAE will ultimately lie. At the same time, Abu Dhabi’s ADGM continues to post exceptional growth figures, rapidly expanding its footprint, licence base and institutional influence.

What is unfolding is not a simple rivalry. It is a strategic tug-of-war between two emirates with very different economic DNA, each seeking to position itself as the leading hub for global finance and next-generation technology. This competition carries significant implications not only for businesses choosing where to locate but also for real estate markets across Dubai, Abu Dhabi, and the wider region.

Understanding DIFC and ADGM requires looking beyond headline numbers to how each ecosystem has evolved, what each does best, and whether the dual-hub model strengthens the UAE or risks internal fragmentation.

The rise of DIFC as a global financial centre began in 2004, when Dubai made a decisive move to position itself as a bridge between East and West. DIFC was built on English common law principles, offered regulatory independence and world-class infrastructure, and was deliberately designed to attract international banks, asset managers, insurers and professional services firms.

Over two decades, DIFC has grown into one of the most recognisable financial centres outside London, New York and Hong Kong. Its ecosystem now includes thousands of companies across banking, asset management, hedge funds, private equity, fintech, digital assets, legal services and consultancies. Crucially, DIFC has never been just a financial district. It has evolved as an urban centre, integrating offices, galleries, restaurants, residences and cultural institutions into a single high-density business environment.

The latest expansion announcement represents a new chapter. DIFC’s next phase is not simply about adding office towers. It is about creating an innovation-led district that integrates AI campuses, technology clusters, educational institutions, residential neighbourhoods and lifestyle assets. This signals Dubai’s intention to future-proof DIFC by embedding technology and liveability into its core value proposition.

ADGM, by contrast, is the newer entrant. Fully operational since 2015, it was conceived with a different strategic lens. Abu Dhabi did not need to prove its relevance as a global city. Its competitive advantage lay in capital depth, institutional stability and long-term investment power. ADGM was therefore designed to attract institutional finance, asset managers, family offices, fintech firms and regulated digital asset businesses seeking a robust, globally aligned legal framework.

In less than a decade, ADGM has grown at remarkable speed. Its jurisdiction now spans both Al Maryah Island and Al Reem Island, giving it a much larger physical footprint than DIFC. Licence issuance has surged, making ADGM one of the fastest-growing international financial centres globally. More importantly, it has positioned itself as a trusted base for institutional capital, supported by Abu Dhabi’s sovereign wealth ecosystem.

While DIFC and ADGM share similarities in legal structure and regulatory independence, their strategic positioning differs in important ways.

DIFC’s strength lies in scale, diversity and global connectivity. It directly benefits from Dubai’s role as an international travel hub, lifestyle destination, and business gateway. For international firms entering the Middle East, DIFC often feels like the most familiar and accessible starting point. Its density of professional services, talent, and deal flow creates powerful network effects.

ADGM’s strength lies in depth and alignment with long-term capital. Abu Dhabi is home to some of the largest sovereign wealth funds in the world, managing trillions of dollars. The proximity of these institutions to ADGM provides an implicit signal of stability and seriousness that appeals to global asset managers and institutional investors. ADGM has also been particularly proactive in regulating emerging sectors such as digital assets, providing clarity where many jurisdictions remain cautious.

When assessing who holds the upper hand, the answer depends entirely on the metric used.

In terms of brand recognition and ecosystem maturity, DIFC remains the leader. Its name carries global weight, and its concentration of international banks, hedge funds and professional firms remains unmatched in the region. Dubai’s aggressive expansion strategy reinforces this advantage by ensuring DIFC remains relevant as finance becomes increasingly intertwined with technology and AI.

In terms of growth momentum and institutional alignment, ADGM is arguably ahead. Its licence growth, expansion into new districts and increasing dominance in asset management suggest a centre that is still accelerating. For firms prioritising regulatory clarity, access to long-term capital and a more measured growth environment, ADGM is increasingly compelling.

Rather than one clearly overtaking the other, what is emerging is a form of competitive specialisation. DIFC is becoming the natural home for innovation-led finance, fintech, AI-driven businesses and global entrepreneurial capital. ADGM is positioning itself as the institutional heart of the UAE’s financial system, deeply integrated with sovereign capital and long-term investment strategies.

This competition raises an important question: is having two rival financial centres good for the UAE, or does it risk diluting impact?

Historically, competition between cities and financial hubs has often strengthened national economies rather than weakened them. London and New York, Singapore and Hong Kong, Frankfurt and Paris all demonstrate that multiple centres can coexist while pushing each other to improve. In the UAE, DIFC and ADGM are forcing each other to innovate faster, refine regulations, improve infrastructure, and attract global talent more aggressively.

For businesses, this means more choice, better incentives and higher-quality ecosystems. Firms can select environments that best suit their operational model, whether that is fast-moving innovation or institutionally anchored finance. For the UAE as a whole, it reduces dependency on a single centre and increases resilience.

However, the risks should not be ignored. Overlapping strategies could lead to infrastructure duplication and talent competition. If both hubs chase the same firms without differentiation, wage inflation and talent shortages could emerge. Regulatory divergence, if unmanaged, could also create friction for firms operating across both jurisdictions.

The key to long-term success lies in coordination rather than consolidation. As long as DIFC and ADGM continue to specialise while aligning on overarching national objectives, the competition remains healthy.

One of the most immediate and tangible consequences of this power dynamic is its impact on real estate.

In Dubai, DIFC’s expansion is already reshaping demand patterns. Prime office space in and around DIFC remains extremely short in supply, pushing rents higher and driving demand into adjacent districts such as Downtown Dubai and Business Bay. The integration of residential developments within DIFC itself has added a new layer to the market, with premium pricing reflecting both scarcity and lifestyle appeal.

As DIFC expands physically, the knock-on effect for Dubai’s wider property market is significant. High-income professionals, entrepreneurs, and executives drawn to finance and technology roles are increasing demand for luxury and mid-to-high-end residential stock. Retail, hospitality, and mixed-use developments benefit from increased footfall and spending power. Over time, this supports sustained capital value appreciation rather than speculative spikes.

In Abu Dhabi, ADGM’s growth has had an equally profound impact, albeit with a different character. Office demand around Al Maryah and Al Reem Islands has strengthened considerably, with limited high-quality supply supporting rental growth. Residential demand has followed, particularly in waterfront and centrally located developments favoured by professionals and institutional employees.

Abu Dhabi’s more controlled development pipeline has led to greater price stability than Dubai’s historically cyclical market. For long-term investors, this measured growth profile, combined with ADGM’s institutional gravity, has become increasingly attractive.

Beyond the two cities, there are broader regional implications. A strong, competitive UAE financial ecosystem enhances the country’s position as a gateway to the Middle East, Africa and South Asia. This benefits not only Dubai and Abu Dhabi, but also neighbouring markets that interact with UAE-based capital, talent and institutions. The rising sophistication of the UAE’s financial hubs also raises benchmarks across the GCC, influencing how cities such as Riyadh position their own financial districts.

Looking ahead, the most likely outcome is not a decisive victory for DIFC or ADGM, but a dual-leadership model. Dubai will continue to dominate in global connectivity, innovation-led finance and lifestyle-driven talent attraction. Abu Dhabi will consolidate its role as the institutional and capital-anchored centre of the UAE’s financial system.

For investors, developers and businesses, this is a net positive. It means deeper markets, more resilient growth drivers and diversified real estate demand across multiple cities. The real risk would not be competition, but complacency.

In that sense, the DIFC-ADGM dynamic may prove to be one of the UAE’s greatest strategic strengths.ns remain supportive.

Discover the best Dubai Off Plan Investments on these links, including Trump Tower Dubai, Lumena Alta and Jumeriah Residence Emirate Towers DIFC

Please enter your details to register your interest. Our investment expert will contact you to discuss the various opportunities, along with unit pricing and availability.

Off Plan Dubai

Suite: 508, Fairmont,

Sheikh Zayed Road,

P O Box 75671,

Dubai, UAE

Off Plan Dubai

167–169 Great Portland Street, 5th Floor, London, W1W 5PF.

The floor plans and brochure for this development will be emailed to you once you request further information from us.