We are back in Dubai today. As we have consistently highlighted this year, if you are buying off-plan, it has never been more important to be selective and disciplined in choosing the right opportunities. Market depth has increased, supply is more nuanced, and not all launches will perform equally over the next cycle. You need to be protected from market corrections, oversupply, price fluctuations, and broader economic conditions.

Our core apartment focus for 2026 sits firmly in two locations. ADGM in Abu Dhabi and the expansion of DIFC into DIFC 2 and Zabeel in Dubai. These are not lifestyle-driven decisions. They are driven by employment density, institutional demand, purposeful sustained undersupply, and long-term capital protection.

Earlier today, we attended the international investor briefing to announce DIFC 2. The expansion is material in scale and strategic in intent. It effectively extends the existing DIFC financial district into a new mixed-use urban quarter, creating additional capacity for global financial institutions, professional services firms, technology companies, and regional AI headquarters.

DIFC 2 is not simply an overspill of office space. It is designed as a fully integrated live-work environment, incorporating Grade A commercial space, innovation hubs, hospitality, retail, cultural venues, and a carefully planned residential component. This structure is critical because it anchors residential demand in real economic activity rather than speculative lifestyle trends.

For investors, the most important takeaway from today’s briefing is the first residential launch in DIFC 2: The Residences, in Phase A of the development, which is expected to be ready by 2030.

The Residences, comprising two mid-rise towers, are the flagship residential offering of the new district and set the benchmark for quality, pricing, and long-term value across DIFC 2. These homes are designed specifically for DIFC professionals, senior executives, and international talent who seek proximity to their workplaces while maintaining a high standard of living.

Architecturally, the development is contemporary and distinctive, with residences positioned to capture expansive views across Dubai’s key landmarks. The arrival experience is hospitality-inspired, with refined lobby and lounge spaces designed for both privacy and informal interaction. Shared workspaces and social spaces are integrated throughout, reflecting how modern professionals live and work.

Lifestyle and wellness have been thoughtfully incorporated. Residents will have access to a two-kilometre inner green circle, providing landscaped walkways for walking, jogging, and relaxation. The development also features thematic water elements that enhance a sense of calm within an otherwise high-energy financial district.

Amenities are comprehensive and purposeful. These include a resort-style pool with cabanas, a separate family pool with a children’s splash pad, a fully equipped clubhouse with gym and yoga studio, padel and squash courts, and a range of social and recreational spaces. Premium retail and destination food and beverage offerings are embedded within the wider DIFC 2 masterplan, ensuring convenience without compromising quality.

From an investment perspective, The Residences benefit from a clear first-mover advantage. As the inaugural residential launch within DIFC 2, pricing reflects an early-stage entry point before the district is fully established. Historically, first launches within landmark financial districts tend to outperform subsequent phases as infrastructure is delivered, demand intensifies, and pricing resets upwards.

We are the strongest advocates for purchasing in the first phases; all future phases will have incremental price increases, and you are not reliant on external market growth to ride appreciation waves.

Pricing for The Residences is approximately 4,000 AED per square foot, with starting units priced from 2.6 million AED. The booking process opens today. Expressions of Interest should be submitted through our team, and unit selection will take place on the 12th of February. With only 496 units across the two towers, it is essential to act quickly to secure the most desirable options.

Neda, the Sales Director for the developer, will be overseeing the process, while Savills is personally managing all Off-Plan Dubai clients. This ensures every investor can access preferred units and secure early-stage pricing before the district is fully established.

Rental demand is expected to be robust and resilient. The target tenant profile includes partners at financial and legal firms, regional directors, C-suite executives, and long-term expatriates. This supports strong occupancy, premium rents, and lower volatility compared to lifestyle-led residential markets.

Supply within DIFC and DIFC 2 remains intentionally limited. This constraint, combined with growing employment density, underpins long-term capital appreciation and provides downside protection that is increasingly important in the current market.

We believe DIFC 2 and The Residences sit firmly in the category of strategic, fundamentals-driven investments rather than speculative off-plan purchases. For investors seeking exposure to Dubai with a focus on yield quality, tenant depth, and capital preservation, this location deserves close attention. As an advisory, we are as confident as possible that, at this price point, these apartments will outperform nearly all contemporaries and alternatives launching in 2026.

For buyers entering at this stage, The Residences offer the opportunity to secure property at the foundation of Dubai’s next major growth cycle. Whether the objective is income generation, long-term capital appreciation, or securing a strategic home in the heart of the city, this first launch represents a rare alignment of location, demand, and timing.

Dubai International Financial Centre (DIFC) is a federal financial free zone within Dubai. Legally, it is not subject to UAE civil law in nearly all commercial matters. DIFC operates under English Common Law and not UAE civil law, hence the different registration fees of 5% and not the usual 4%

How the Launch of DIFC 2 and Its Expansion Will Influence Dubai as a Region

The launch of DIFC 2 and the broader expansion of the Dubai International Financial Centre mark a defining moment not only for Dubai but also for the economic trajectory of the Middle East. This is not a conventional real estate expansion or a simple increase in office supply. It represents a strategic recalibration of Dubai’s role in global finance, talent attraction, capital flows and regional leadership.

DIFC has already established itself as the leading financial centre across the Middle East, Africa and South Asia. The expansion, often referred to as DIFC 2 or the Zabeel District, takes that foundation and scales it to a level that places Dubai firmly in competition with the world’s most established financial capitals. The implications extend well beyond the district, influencing employment, real estate markets, investment behaviour, and Dubai’s long-term economic resilience.

A Structural Upgrade to Dubai’s Financial Ecosystem

At its core, DIFC 2 is about capacity and evolution. The original DIFC reached maturity faster than many expected, driven by an influx of global banks, asset managers, hedge funds, fintech firms, insurers and family offices. Demand for high-quality office space, regulated financial infrastructure and specialist talent has consistently outpaced supply.

The expansion dramatically increases DIFC’s physical footprint, creating space for thousands of additional firms and tens of thousands of new professionals. More importantly, it allows Dubai to diversify the types of institutions and activities it can host. DIFC 2 is designed to support not only traditional finance, but also private capital, venture funding, artificial intelligence, digital assets, sustainability-focused finance and next-generation financial services.

This shift strengthens Dubai’s position as a full-spectrum financial hub rather than a regional outpost. As global financial institutions increasingly look to diversify their geographic exposure, DIFC 2 positions Dubai as a credible long-term base rather than a satellite office.

Economic Diversification and Long-Term Growth

Dubai’s economic strategy has long focused on reducing dependence on cyclical sectors and building a resilient, knowledge-based economy. DIFC 2 fits directly into this ambition.

The scale of investment behind the expansion signals long-term confidence in Dubai’s ability to attract global capital and talent. By creating an environment where finance, technology, education and innovation coexist, Dubai is anchoring future economic growth in high-value sectors that are less vulnerable to commodity cycles or regional volatility.

The ripple effect extends into professional services, legal frameworks, consulting, education, hospitality and lifestyle industries. As financial institutions expand, they draw in a network of supporting industries, reinforcing Dubai’s role as a self-sustaining economic ecosystem rather than a single-sector city.

Talent Attraction, Retention and Global Mobility

One of the most transformative aspects of DIFC 2 is its focus on people, not just companies. The expansion integrates office space with residential, retail, cultural and educational components, creating an environment designed to retain talent rather than simply attract it.

In a global economy where highly skilled professionals can choose between multiple international hubs, lifestyle plays a decisive role. DIFC 2 responds to this by offering a live-work-play model that reduces friction between professional and personal life. This makes Dubai more competitive against cities such as London, Singapore and New York, particularly for younger professionals and entrepreneurs.

Education and professional development are also embedded into the plan, strengthening Dubai’s ability to cultivate local and regional talent alongside international expertise. Over time, this reduces reliance on imported talent and creates a more sustainable, locally anchored workforce.

Capital Flows and Institutional Investment

The expansion of DIFC significantly enhances Dubai’s ability to capture global capital flows. As financial firms cluster, liquidity increases, deal flow accelerates and confidence compounds. This creates a virtuous cycle in which Dubai becomes not just a destination for capital, but a place where capital is actively deployed across the region.

Private equity, venture capital, family offices and sovereign wealth-linked entities are particularly drawn to jurisdictions that offer regulatory clarity, political stability and global connectivity. DIFC 2 strengthens all three pillars. As a result, Dubai’s influence over regional investment decisions is likely to increase, with capital routed through DIFC into markets across the Middle East, Africa and South Asia.

This has strategic implications beyond economics. Cities that control capital flows gain disproportionate influence over regional development, innovation and corporate strategy.

Real Estate Potential and Investor Opportunity

The real estate implications of DIFC 2 are among the most significant and far-reaching aspects of the expansion, creating both direct and indirect opportunities for investors.

At the core level, DIFC 2 introduces a large volume of new mixed-use real estate in one of Dubai’s most supply-constrained and prestigious zones. Office space within DIFC has historically commanded premium rents due to limited availability, regulatory advantages and proximity to decision-makers. While the expansion increases supply, it also fundamentally expands demand by attracting new categories of firms and institutions that previously could not be accommodated.

Grade A office assets within and adjacent to DIFC 2 are likely to remain structurally undersupplied relative to long-term demand. This supports rental resilience and positions prime commercial assets as long-duration income investments rather than cyclical plays. Institutional investors, sovereign funds and family offices are likely to target these assets for capital preservation and steady yield rather than speculative appreciation alone.

On the residential side, DIFC 2 will significantly influence demand patterns across surrounding districts. Financial professionals, executives and international talent typically seek proximity to work, high-quality amenities and lifestyle infrastructure. This drives sustained demand for premium residential units in neighbouring areas, including Downtown Dubai, Business Bay, Zabeel, Al Jaddaf, and emerging mixed-use corridors.

As employment density increases, rental demand is expected to remain strong, particularly for well-designed one- and two-bedroom units suited to professionals and expatriate households. This creates attractive conditions for buy-to-let investors, especially those targeting long-term income rather than short-term speculation.

There is also a secondary effect on land values and redevelopment opportunities. Areas previously considered transitional or secondary may benefit from re-rating as connectivity, infrastructure, and prestige improve. Savvy investors may find opportunities in assets just outside the core DIFC zone that benefit from its gravitational pull.

Importantly, DIFC 2 reinforces Dubai’s appeal to institutional real estate capital. Pension funds, insurance companies and global property investors increasingly prioritise cities with strong employment fundamentals, transparent regulation and international tenant demand. DIFC 2 strengthens Dubai’s credentials across all three, supporting deeper and more stable real estate capital inflows over the coming decade.

Spillover Effects on the Wider Urban Landscape

Beyond direct investment zones, DIFC 2 influences how Dubai evolves spatially. As the financial district expands westward and integrates with surrounding neighbourhoods, it reshapes commuting patterns, infrastructure priorities and urban density.

This supports further investment in transport, public spaces and mixed-use developments, enhancing overall urban efficiency. Over time, this reduces the city’s reliance on long commutes and fragmented zoning, improving quality of life and economic productivity.

Retail, hospitality and leisure assets also benefit as footfall increases and spending power concentrates around the expanded district. These sectors often experience some of the earliest uplift following major employment-led developments.

Regional Positioning and Competitive Advantage

The expansion of DIFC must also be viewed in a regional context. Across the Gulf, major cities are competing to attract multinational headquarters, financial institutions and global talent. DIFC 2 is a clear signal that Dubai intends to defend and extend its first-mover advantage.

By scaling faster and more comprehensively than competitors, Dubai increases the cost of switching for firms already established in the ecosystem. Once companies embed themselves within a dense network of regulators, service providers, talent and capital, relocation becomes less attractive.

This strengthens Dubai’s long-term dominance as the region’s primary international business hub, even as other cities grow in parallel.

Long-Term Strategic Impact

DIFC 2 is not designed as a short-term economic stimulus. Its phased development timeline reflects a long-range view of Dubai’s future, extending well into the 2030s and beyond. This long-term planning reduces the risk of oversupply and aligns development with real demand growth.

As the expansion matures, DIFC is likely to evolve from a financial district into a fully integrated economic city within a city, shaping Dubai’s identity for decades. The cumulative effect will be a deeper, more diversified economy that is less sensitive to global shocks and more embedded in international systems.

Conclusion

The launch of DIFC 2 and the expansion of the Dubai International Financial Centre represent a structural shift in Dubai’s economic model. It strengthens Dubai’s role as a global financial hub, accelerates economic diversification, attracts and retains international talent, and unlocks significant real estate investment opportunities.

For investors, DIFC 2 is not just about new buildings but about participating in the long-term growth of a city positioning itself as a permanent centre of global capital. For Dubai, it is a decisive step toward securing its place among the world’s most influential economic cities.

DIFC vs ADGM: The UAE’s Financial and Tech Power Struggle and What It Means for Business and Real Estate

The United Arab Emirates is in the middle of a defining economic shift. Finance, artificial intelligence, technology, and global capital flows are converging at speed, and the country’s ambition is no longer regional leadership alone, but genuine global relevance. At the centre of this transformation sit two powerful financial free zones: Dubai International Financial Centre and Abu Dhabi Global Market.

Dubai’s recent announcement of a major extension to DIFC, with a second phase estimated to exceed one hundred billion dollars in total investment value, has reignited debate about where the true centre of gravity for finance, AI and technology in the UAE will ultimately lie. At the same time, Abu Dhabi’s ADGM continues to post exceptional growth figures, rapidly expanding its footprint, licence base and institutional influence.

What is unfolding is not a simple rivalry. It is a strategic tug-of-war between two emirates with very different economic DNA, each seeking to position itself as the leading hub for global finance and next-generation technology. This competition carries significant implications not only for businesses choosing where to locate but also for real estate markets across Dubai, Abu Dhabi, and the wider region.

Understanding DIFC and ADGM requires looking beyond headline numbers to how each ecosystem has evolved, what each does best, and whether the dual-hub model strengthens the UAE or risks internal fragmentation.

The rise of DIFC as a global financial centre began in 2004, when Dubai made a decisive move to position itself as a bridge between East and West. DIFC was built on English common law principles, offered regulatory independence and world-class infrastructure, and was deliberately designed to attract international banks, asset managers, insurers and professional services firms.

Over two decades, DIFC has grown into one of the most recognisable financial centres outside London, New York and Hong Kong. Its ecosystem now includes thousands of companies across banking, asset management, hedge funds, private equity, fintech, digital assets, legal services and consultancies. Crucially, DIFC has never been just a financial district. It has evolved as an urban centre, integrating offices, galleries, restaurants, residences and cultural institutions into a single high-density business environment.

The latest expansion announcement represents a new chapter. DIFC’s next phase is not simply about adding office towers. It is about creating an innovation-led district that integrates AI campuses, technology clusters, educational institutions, residential neighbourhoods and lifestyle assets. This signals Dubai’s intention to future-proof DIFC by embedding technology and liveability into its core value proposition.

ADGM, by contrast, is the newer entrant. Fully operational since 2015, it was conceived with a different strategic lens. Abu Dhabi did not need to prove its relevance as a global city. Its competitive advantage lay in capital depth, institutional stability and long-term investment power. ADGM was therefore designed to attract institutional finance, asset managers, family offices, fintech firms and regulated digital asset businesses seeking a robust, globally aligned legal framework.

In less than a decade, ADGM has grown at remarkable speed. Its jurisdiction now spans both Al Maryah Island and Al Reem Island, giving it a much larger physical footprint than DIFC. Licence issuance has surged, making ADGM one of the fastest-growing international financial centres globally. More importantly, it has positioned itself as a trusted base for institutional capital, supported by Abu Dhabi’s sovereign wealth ecosystem.

While DIFC and ADGM share similarities in legal structure and regulatory independence, their strategic positioning differs in important ways.

DIFC’s strength lies in scale, diversity and global connectivity. It directly benefits from Dubai’s role as an international travel hub, lifestyle destination, and business gateway. For international firms entering the Middle East, DIFC often feels like the most familiar and accessible starting point. Its density of professional services, talent, and deal flow creates powerful network effects.

ADGM’s strength lies in depth and alignment with long-term capital. Abu Dhabi is home to some of the largest sovereign wealth funds in the world, managing trillions of dollars. The proximity of these institutions to ADGM provides an implicit signal of stability and seriousness that appeals to global asset managers and institutional investors. ADGM has also been particularly proactive in regulating emerging sectors such as digital assets, providing clarity where many jurisdictions remain cautious.

When assessing who holds the upper hand, the answer depends entirely on the metric used.

In terms of brand recognition and ecosystem maturity, DIFC remains the leader. Its name carries global weight, and its concentration of international banks, hedge funds and professional firms remains unmatched in the region. Dubai’s aggressive expansion strategy reinforces this advantage by ensuring DIFC remains relevant as finance becomes increasingly intertwined with technology and AI.

In terms of growth momentum and institutional alignment, ADGM is arguably ahead. Its licence growth, expansion into new districts and increasing dominance in asset management suggest a centre that is still accelerating. For firms prioritising regulatory clarity, access to long-term capital and a more measured growth environment, ADGM is increasingly compelling.

Rather than one clearly overtaking the other, what is emerging is a form of competitive specialisation. DIFC is becoming the natural home for innovation-led finance, fintech, AI-driven businesses and global entrepreneurial capital. ADGM is positioning itself as the institutional heart of the UAE’s financial system, deeply integrated with sovereign capital and long-term investment strategies.

This competition raises an important question: is having two rival financial centres good for the UAE, or does it risk diluting impact?

Historically, competition between cities and financial hubs has often strengthened national economies rather than weakened them. London and New York, Singapore and Hong Kong, Frankfurt and Paris all demonstrate that multiple centres can coexist while pushing each other to improve. In the UAE, DIFC and ADGM are forcing each other to innovate faster, refine regulations, improve infrastructure, and attract global talent more aggressively.

For businesses, this means more choice, better incentives and higher-quality ecosystems. Firms can select environments that best suit their operational model, whether that is fast-moving innovation or institutionally anchored finance. For the UAE as a whole, it reduces dependency on a single centre and increases resilience.

However, the risks should not be ignored. Overlapping strategies could lead to infrastructure duplication and talent competition. If both hubs chase the same firms without differentiation, wage inflation and talent shortages could emerge. Regulatory divergence, if unmanaged, could also create friction for firms operating across both jurisdictions.

The key to long-term success lies in coordination rather than consolidation. As long as DIFC and ADGM continue to specialise while aligning on overarching national objectives, the competition remains healthy.

One of the most immediate and tangible consequences of this power dynamic is its impact on real estate.

In Dubai, DIFC’s expansion is already reshaping demand patterns. Prime office space in and around DIFC remains extremely short in supply, pushing rents higher and driving demand into adjacent districts such as Downtown Dubai and Business Bay. The integration of residential developments within DIFC itself has added a new layer to the market, with premium pricing reflecting both scarcity and lifestyle appeal.

As DIFC expands physically, the knock-on effect for Dubai’s wider property market is significant. High-income professionals, entrepreneurs, and executives drawn to finance and technology roles are increasing demand for luxury and mid-to-high-end residential stock. Retail, hospitality, and mixed-use developments benefit from increased footfall and spending power. Over time, this supports sustained capital value appreciation rather than speculative spikes.

In Abu Dhabi, ADGM’s growth has had an equally profound impact, albeit with a different character. Office demand around Al Maryah and Al Reem Islands has strengthened considerably, with limited high-quality supply supporting rental growth. Residential demand has followed, particularly in waterfront and centrally located developments favoured by professionals and institutional employees.

Abu Dhabi’s more controlled development pipeline has led to greater price stability than Dubai’s historically cyclical market. For long-term investors, this measured growth profile, combined with ADGM’s institutional gravity, has become increasingly attractive.

Beyond the two cities, there are broader regional implications. A strong, competitive UAE financial ecosystem enhances the country’s position as a gateway to the Middle East, Africa and South Asia. This benefits not only Dubai and Abu Dhabi, but also neighbouring markets that interact with UAE-based capital, talent and institutions. The rising sophistication of the UAE’s financial hubs also raises benchmarks across the GCC, influencing how cities such as Riyadh position their own financial districts.

Looking ahead, the most likely outcome is not a decisive victory for DIFC or ADGM, but a dual-leadership model. Dubai will continue to dominate in global connectivity, innovation-led finance and lifestyle-driven talent attraction. Abu Dhabi will consolidate its role as the institutional and capital-anchored centre of the UAE’s financial system.

For investors, developers and businesses, this is a net positive. It means deeper markets, more resilient growth drivers and diversified real estate demand across multiple cities. The real risk would not be competition, but complacency.

In that sense, the DIFC-ADGM dynamic may prove to be one of the UAE’s greatest strategic strengths.ns remain supportive.

Off Plan Dubai are experts in spotting the best value options in the Dubai Real Estate market

Dear Investors,

I hope you are all doing well.

Firstly, thank you to everyone who participated in the launches across Saudi Arabia over the past week. The response has been exceptional, and I genuinely appreciate the trust you continue to place in us. There are still a limited number of opportunities available, so if you have been considering getting in touch, now is the right time.

Today, I want to highlight a very special opportunity in Dubai. As many of you know, I believe the lower and lower-mid apartment segment will come under increasing pressure in 2026 due to supply. This year, there are only a handful of projects I would confidently recommend, and I expect to be able to count them on one hand.

The segment that will continue to outperform is the high-end luxury market. This is where we still see genuine value, sustained appreciation, and strong international demand, combined with a lack of live, high-quality stock to adequately service that demand.

Omniyat remains the undisputed leader in Dubai’s high-end real estate sector, and Marasi Bay has firmly established itself as the UHNW location of choice, alongside Palm Jumeirah.

Our approach has always been simple: identify true value. That is where real returns are made, and where long-term relationships built on trust and knowledge are formed. In this instance, we have genuinely hit the jackpot.

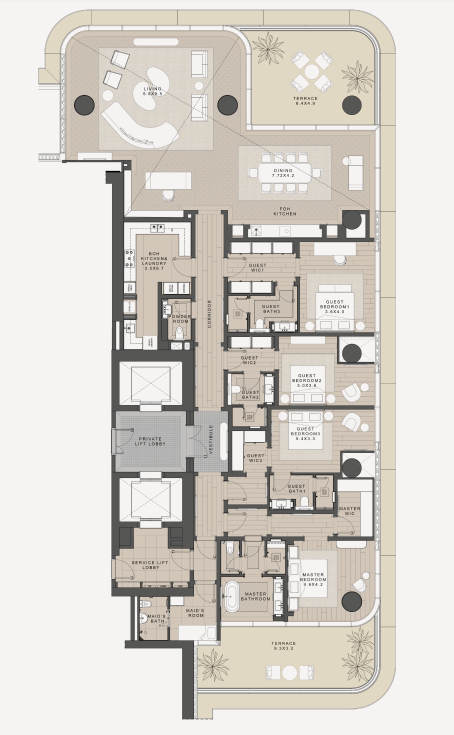

Vela Viento.

The jewel in the Marasi Bay crown, Vela Viento, is managed by the world-renowned Dorchester Collection. During the launch phase, we successfully sold multiple apartments, with two-bedroom units averaging between AED 20–25 million and four-bedroom duplexes achieving AED 60–80 million on capital-forward payment terms. The building itself is exceptional in every sense.

Every residence represents the pinnacle of design and luxury, with interiors by Gilles & Boissier. Originally, the top two floors were planned as a single ultra-exclusive full-floor duplex penthouse, valued at approximately AED 258 million, intended to rival Dubai’s all-time penthouse record.

This week, Omniyat made a strategic decision to restructure that offering to appeal to the wider UHNW market rather than only billionaire buyers. As a result, the top floor has now been divided into two penthouses.

The opportunity I am presenting is the absolute top penthouse within the building.

It is a four-bedroom, five-bathroom residence, priced at just AED 40 million. Crucially, for January only, it is available on a highly attractive 30/70 payment plan rather than the standard 60/40 structure. This means only AED 12 million is payable between now and handover in December 2027.

Based on completed RICS valuations and comparable delivered Dorchester residences, this structure alone delivers a projected return of over 100% on capital deployed.

This unit was not available at launch. Quite simply, it did not exist in its current configuration. Had it been released originally, it would have sold immediately to any investor capable of quickly identifying value through floor plans and massing. An absolute top-floor four-bedroom penthouse at AED 40 million, approximately AED 20 million below mid-floor duplex pricing, is a no-brainer from an investment perspective.

For a fully furnished Dorchester-managed penthouse at the very top of Vela Viento, with a completed valuation in excess of AED 58 million, this represents a truly exceptional opportunity.

In off-plan investments, I typically advise holding through to handover to maximise appreciation. However, this unit is fundamentally undervalued. Approximately six months prior to completion, I would recommend positioning it as a true penthouse resale, at which point Dorchester-branded residences historically gain significant traction with end users.

The 30/70 payment plan provides an additional strategic advantage. Future buyers can acquire the unit by paying the original 30% plus appreciation, with the remaining balance financed. This effectively halves the capital required compared to comparable units on a 60/40 structure, giving this penthouse a decisive edge in the resale market.

Between the floor position, pricing, payment terms, branding, and valuation gap, this is one of the strongest luxury off-plan opportunities I have seen in Dubai in recent years.

NEW UNIT RELEASE AS OF TODAY

🔥VELA VIENTO – UNIT 4001 (Top Floor Unit)🔥

This is an incredible opportunity to secure the newly released, top-floor unit at our Dorchester Collection development, VELA VIENTO, situated in the heart of Marasi Bay.

This unit has not been on the market before, and we are delighted to announce that, for Q1 ONLY, we are offering it on a 30/70 payment plan.

Unit Highlights:

* 5,065 sq.ft * Simplex layout with a unique Double Height Living Area * Fully Fitted & Fully Furnished by the world-renowned, Gilles & Boissier * Managed by The Dorchester Collection * Situated in the heart of Marasi Bay * Unrivalled Amenities * Part of Omniyat’s Marasi Bay Master Plan, including The Lana, Vela, Vela Viento, ENARA, Marasi Island, Marasi Sunset Park, and MORE TO COME. * Dual Aspect Views: Burj Khalifa, Marasi Bay Marina, Canal view one side, and the other across Dubai Design District, and The Creek.

AED 40,241,090

Overview of Vela Viento

Vela Viento is an ultra-luxury residential development by Omniyat in Marasi Bay, Business Bay, Dubai. The project is designed by Foster + Partners, with interiors by Gilles & Boissier, and will be managed upon completion by the Dorchester Collection, a globally recognised hospitality brand. It comprises two interconnected towers rising approximately 180 metres with a limited collection of 90–95 exclusive residences, including 2- to 4-bedroom apartments, duplexes, and penthouses. The development is positioned as one of Dubai’s most premium waterfront projects, offering panoramic views of Marasi Bay, Downtown Dubai, and the Burj Khalifa. Vela Viento is scheduled for handover in Q3 2027.

Recent Transaction Levels & Pricing

Because Vela Viento is currently off-plan, there have been no traditional secondary-market transactions with resale data yet. Instead, we rely on launch pricing and early trading figures in Dubai’s off-plan market to understand investor interest and implied valuation trends.

Off-plan prices for Vela Viento start from around AED 18.1 million to AED 20 million for the smaller 2-bedroom units, with larger apartments and penthouses priced significantly higher. Typical 2- to 3-bedroom residences are currently marketed from roughly AED 20 million and up, while 3-bedroom units often trade around the mid-20 million dirham range as pricing matures. At the top end, luxury 4-bedroom duplex units can command prices of AED 60 million to nearly AED 80 million, depending on configuration, reflecting their scale and exclusivity.

There are early analytical estimates that, based on similar luxury launches in Dubai, units purchased today could appreciate by an appreciable amount by the time of handover. One example for a 4-bed apartment suggests a potential rise from around AED 24 million at launch to AED 34–35 million at completion, implying a near 20 percent+ gain over the development period if market conditions remain supportive.

Dubai is currently experiencing not only a residential boom, but also a commercial boom. The number of companies, both Blue-Chip and ambitious SMEs, are moving to the region in numbers that have never been seen before.

One thing Dubai has sorely lacked in previous years is Grade A commercial Office Space. Developers, both Private and government-backed, have focused on Residential projects to bring their visions to life. Commercial buildings have always taken a back seat, until now.

Developers are seeing this opportunity for a growing, thriving commerce sector and, as such, are building buildings to match. Omniyat recently launched Lumena, which brought Grade A facilities and amenities, previously reserved for the most luxurious residential buildings, to the commercial world. The result? Instant Sell out. On the back of the success, we now have Lueman Alta coming, and for our investors, we wanted to take a look at the numbers behind the investment. As smart, private and family money is moving into the Commercial sector in Dubai.

Here is a comprehensive overview of business registration, occupancy, and investment numbers in Dubai’s commercial sector.

Current Occupancy / Vacancy for Grade A Office in Dubai

From recent market reports:

Grade A offices in Dubai are currently experiencing very high occupancy levels, typically around 95%.

In key prime business districts (DIFC, Business Bay, Downtown Dubai, Sheikh Zayed Road, etc.), the occupancy often reaches 95‑98% for high‑spec, Grade A stock.

More widely across Dubai for all office stock, city‑wide occupancy is somewhere in the low 90s percent. Grades B & C are lower but still strong.

The vacancy rate is therefore relatively low for Grade A properties in these prime locations.

In summary, Grade A office space in prime locations in Dubai is highly occupied, with near full utilisation in many cases.

Residential Sector: Occupancy / Yields

For comparison, here are some highlights for the residential side:

Residential occupancy in prime/popular residential areas is also high, often > 90%, particularly in established/freehold communities.

Yields (gross) for residential apartments/studios vary: small units (studios / 1‑beds) tend to give higher yields, sometimes in the ~ 7–9% range in good or mid‑income areas; larger units/villas tend to have lower yields (4‑6%) because of higher acquisition costs.

Investment Comparison: Grade A Offices vs Residential

Here are the pros, cons, and “how they compare” between investing in Grade A offices vs residential in Dubai:

Net Yield / Risk‑Adjusted Return: What the Numbers Imply

Putting together the projections above, here’s how the investment return picture looks, roughly, for Grade A offices vs residential, and what to watch out for. These are estimates rather than precise figures, as much depends on location, tenant quality, financing, costs, and other factors.

How do the current occupancy rates in Grade A offices look, and how does this compare to prime residential areas in Dubai?

Current Occupancy / Vacancy for Grade A Office in Dubai

From recent market reports:

Grade A offices in Dubai are currently experiencing very high occupancy levels, typically around 95%.

In key prime business districts (DIFC, Business Bay, Downtown Dubai, Sheikh Zayed Road, etc.), the occupancy often reaches 95‑98% for high‑spec, Grade A stock.

More widely across Dubai for all office stock, city‑wide occupancy is somewhere in the low 90s percent. Grades B & C are lower but still strong.

The vacancy rate is therefore relatively low for Grade A properties in these prime locations.

In summary, Grade A office space in prime locations in Dubai is very well-occupied, with near full utilisation in many cases.

Residential Sector: Occupancy / Yields

For comparison, here are some highlights for the residential side:

Residential occupancy in prime/popular residential areas is also high, often > 90%, particularly in established/freehold communities.

Yields (gross) for residential apartments/studios vary: small units (studios / 1‑beds) tend to give higher yields, sometimes in the 7–9% range in good or mid‑income areas; larger units/villas tend to have lower yields (4‑6%) because of higher acquisition costs.

Key Takeaways: Which Might Be Better, When?

If you are seeking a higher yield and are comfortable with more concentrated risk, a high capital outlay, and potentially dealing with commercial leases and fit-outs, then Grade A offices in prime locations are highly attractive right now. The very high occupancy and rising rents make the cash flow side promising.

If you prefer lower risk, easier tenant turnover, and possibly a smaller initial investment, then residential might be more appealing. It may yield lower returns (especially for larger units) but offer less volatility and more stable demand.

Also, timing and location matter a lot: Grade A offices in prime nodes (DIFC, Sheikh Zayed Road, Business Bay) are doing much better (higher occupancy, higher rents) than offices in peripheral or older buildings. Similarly, residential in prime areas does well; less so in less desirable or oversupplied areas.

Spotlight: Lumena Alta by Omniyat

Lumena Alta is poised to redefine the future of commercial real estate in Dubai—a 380-metre, mixed-use masterpiece standing alongside Lumena at the gateway to Business Bay.

• Iconic Landmark: by GAD Architects • 380 m | G+72 (73 levels) • 45 floors of premium offices • 16 floors of 5-star luxury hotel • 5 curated retail & F&B outlets • Prime Access & Amenities • 6 basement + 8 podiums • Dedicated entries: Office/Hotel • Fitness & aquatic centre • Business centre • Concierge services

Flexible Floor Plates Floor 3–26: 4,500–5,695 sq ft Floor 27–40: 4,545–6,349 sq ft Floor 41–49: 4,564–7,758 sq ft

Sky Experiences: • Level 56: Triple-height sky lobby with Burj Khalifa views • Rooftop: Tallest skypool in Dubai (355 m) + signature restaurant • Spa & wellness facilities

🚀High ROI potential + strong price appreciation outlook 🌟Rare opportunity to own in an iconic commercial tower in Dubai’s core business district

At Off Plan Dubai, for over 10 years, we have assisted investors, offices and funds in placing capital into some of the most lucrative Off Plan Investments in Dubai and, more recently, other international markets. Our business is now built on referrals and repeat business, which requires a significant level of trust. Ultimately, this means our investors achieve significant Capital Appreciation on the investments they make.

We do this on numerous fronts, and we mean test all investments across a set of fundamentals that you can measure within the market. Firstly, it is essential to understand that Dubai’s property appreciation isn’t random; it tends to follow specific economic, demographic, and policy-driven cycles. We obviously hope you choose to partner with Off Plan Dubai for any future property purchase, but if you wish to understand our process yourself, here are the most impactful factors that cause property values in Dubai to rise, and whether they’re monitorable and predictable:

Key Drivers of Property Appreciation in Dubai:

Population Growth & Inflow of Residents

Dubai’s real estate values rise when population inflows (expats, high-net-worth individuals, new residents through Golden Visas) outpace new supply.

Monitorable? Yes — population growth, visa issuances, and migration trends are reported by the Dubai Statistics Centre and immigration authorities. One of our key population metrics is to calculate the annual number of new residents compared to the number of Off Plan Units sold. For instance, Abu Dhabi currently has 19 new residents for every unit sold.

Supply & Demand Balance

Oversupply has historically slowed appreciation (e.g., 2015–2019), while controlled launches (as seen post-2021) push prices up. In some regions of Dubai, we are currently monitoring a trend of over-launching, which is more prevalent in Master-plans where developers can buy individual plots rather than being fully managed by one leading Master Developer.

Monitorable? ✅ Yes – compare project launches with handovers via DLD (Dubai Land Department) and major consultancies (Knight Frank, CBRE, JLL).

Government Policies & Regulations

Examples: Golden Visa, 100% foreign ownership of companies, retirement visa, and foreign investment reforms. Each policy wave historically boosted demand and prices. These are cross-demographic and impact multiple nationalities.

Monitorable? ✅ Yes – policy announcements are public and often give a lead indicator of demand surges.

Infrastructure & Mega Projects

Big-ticket projects (Palm Jumeirah, Dubai Hills Estate, Rashid Yachts & Marina, Dubai Creek Harbour, Palm Jebel Ali) create long-term appreciation around those zones.

Monitorable? ✅ Yes – Track announced government infrastructure plans and developer masterplans. Examples include extensions of metro lines and multi-million/billion logistics improvements, as seen recently at the entry and exit of Emaar Beachfront, which serves as a strong example.

Interest Rates & Global Liquidity

The UAE dirham is pegged to the USD, so Fed rate cuts/raises directly impact mortgage affordability and investor appetite. The saying goes that the US sneezes and the world catches a cold; this is even more relevant to the UAE, who are pegged against the currency.

Monitorable? ✅ Yes — follow US Fed policy and UAE Central Bank rate moves.

Investor Sentiment & Global Capital Flows

Dubai attracts inflows when there’s instability elsewhere (Russia-Ukraine, high taxation in Europe, currency devaluation in Asia). Dubai is exceptional at proving to be a haven when turmoil hits other regions. A super strong, decisive leadership, as seen through COVID-19, and a low-tax, tax-free society that rewards entrepreneurs and innovators, the world’s talent sees the UAE and Dubai as a hotspot to flourish.

Monitorable? ⚠️ Partially — geopolitical shocks are unpredictable, but you can track capital flow trends and residency program demand. Although slightly morbid in nature, Dubai is often viewed as a highly safe destination for both the populace and capital in the event of any political conflict or, god-forbid, war.

Tourism & Economic Growth

Dubai’s property cycle aligns with its success as a tourism, trade, and financial hub. More businesses and visitors = higher housing demand.

Monitorable? ✅ Yes – Dubai Tourism (DTCM) stats and GDP growth projections.

Limited Land in Prime Zones

Areas like Palm Jumeirah, Downtown, Jumeirah Bay, and Dubai Hills have scarcity value, creating outsized appreciation compared to emerging zones.

Monitorable? ✅ Yes – supply pipeline shows where scarcity will persist.

Can We Predict Appreciation?

Short-term (1–2 years): Yes, by watching supply handovers, Fed rate policy, and government reforms.

Medium-term (3–5 years): Trends can be modelled based on population inflow vs. supply, but shocks (COVID, oil prices, geopolitics) can change trajectories.

Long-term (10+ years): More predictable in prime and master-planned zones (Palm, Dubai Hills, Creek Harbour) where infrastructure and limited land sustain demand.

Investor Takeaway:

To anticipate appreciation, you want to track three leading indicators consistently:

Supply vs. demand pipeline → handovers vs. visa/population growth.

Global interest rates & liquidity → mortgage and investor flows.

We monitor the above monthly and quarterly, and evaluate the numbers annually. Here is our framework that we send to our investors. For some individual projects, we can identify undervalued projects by comparing the price per sqft at launch to real-life comparables. We like to incorporate this process into the framework below.

Dubai Property Appreciation Watchlist Framework:

1. Demand-Side Indicators Why it matters: Rising demand without equivalent supply = appreciation.

Population growth & new visas issued.

Sources: Dubai Statistics Centre, GDRFA, press releases on Golden Visa/Residency Visa uptake.

What to watch: Quarterly inflow of new residents; high spikes indicate demand surges.

Foreign direct investment in real estate

Sources: Dubai Land Department (DLD) reports, Knight Frank, CBRE.

What to watch: Nationalities leading purchases (e.g., Russians 2022–23, Indians, Chinese, Europeans).

Tourism numbers

Sources: DTCM reports.

What to watch: Hotel occupancy & visitor count (short-term rental demand).

Quarterly: Review population inflows, tourism data, and handover vs. launch balance.

Annually: Assess mega-project completions, supply pipeline, and global capital inflows.

The Dubai market has provided opportunities since COVID that have literally changed people’s financial lives. Investors are now naturally wondering if the opportunity has passed them by or if there are still opportunities and potential to make solid money over the coming years. We have gone through the first half of the year, and here is a clean, data-driven read on H1-2025 and what it signals for H2-2025 into 2026.

Where transactions were heaviest (H1-2025)

Top areas by number of deals (DLD data):

Al Barsha South Fourth – 10,469

Al Yalayis 1 – 7,595

Wadi Al Safa 5 – 7,178

Next tier included Business Bay (6,601), Dubai Marina (6,428), Airport City (5,569), Jebel Ali First, Al Thanyah Fifth, Burj Khalifa (Downtown), Meaisem First.

Top areas by value (H1-2025):

Dubai Marina – AED 25.1bn

Business Bay – AED 22.5bn

Burj Khalifa (Downtown Dubai) – AED 17.1bn

Palm Jumeirah – AED 16.96bn (also high: Al Yalayis 1, Meaisem Second, Wadi Al Safa 5, Airport City, Al Barsha South Fourth).

Big H1-2025 market signals (headline numbers):

Record half-year: total real-estate procedures exceeded AED 431bn, with circa 99k sales and strong investor participation.

Off-plan continued to lead the way (circa 65%+ share by count) with apartments accounting for 80% of deals; meanwhile, secondary gained momentum.

Price growth is still positive (values up ~14% y/y to June), but it is more segmented by community.

Supply pressure: 20k+ units delivered in H1, with a large handover wave expected in H2; pipeline 200k+ through 2027. Completions concentrated in JVC, Sobha Hartland, and MBR City. We have continued to speak about trepidation in areas with high concentrations of handovers.

DXBinteract mid-year: transactions +22.5% y/y by count, +40% by value; mortgages up by volume but lower average ticket, more cash but placed on smaller loans.

Hot Locations:

Value magnets: Marina, Business Bay, Downtown/Burj Khalifa, Palm — luxury/brand-led stock, investor depth, and liquidity; these continue to set the pace for AED value.

Volume workhorses: Al Barsha South Fourth, Al Yalayis 1, Wadi Al Safa 5 — areas with heavy off-plan launches and mid-market price points (broad buyer pools, investor-friendly ticket sizes). At Off Plan Dubai, we do not cover these areas, but appreciate the ‘bulk’ of the market they provide.

Affordable/mid-market momentum: JVC/Arjan/Dubailand corridors saw big handovers and sales churn; this is where any supply-driven price moderation shows up first.

What to watch out for in H2-2025 → 2026

1) Supply digestion vs. price growth

The handover bulge in H2 (after 20k+ in H1) should cool quarterly price growth for mid-market apartments in outer corridors; expect more competitive pricing & incentives from developers. Prime/luxury remains more resilient but likely slower growth off a higher base.

2) Off-plan still dominant, but resale continues its race to catch up:

DXBinteract shows secondary prices rising faster y/y than off-plan in several segments; that can keep ready units in mature family communities (e.g., Dubai Hills, Arabian Ranches, Jumeirah Park) in demand. DXB Interact

3) Financing mix

Mortgage counts up, values down → more cash buyers/smaller LTVs. If rates ease into 2026, you could see resale liquidity improve and upgrade activity pick up.

4) Infrastructure catalysts

DWC/Al Maktoum Airport expansion and Dubai South narrative continue to build; land/early-phase townhouse projects there should see sustained enquiry.

5) Leasing

Rent growth moderating from 2023–24 highs as supply lands, especially in studios/1-beds; villa rents remain stickier due to scarcer stock. (

Strategy for an investor (actionable):

Hold/accumulate in value-dense, liquid cores (Marina, Business Bay, Downtown micro-units with strong STR/long-let demand) for AED value preservation and exit liquidity.

Selective growth in outer mid-market (JVC/Al Barsha South Fourth/Wadi Al Safa 5) after handover waves. Negotiate on post-handover inventory, focus on buildings with proven leasing velocity and realistic service charges.

We have a strong preference for the Villa market, focusing on areas like Polo and The Valley by Emaar.

Resale family villas/townhouses

Target ready units in established school-adjacent communities; these held pricing better in H1 and should remain bid if rates ease in 2026.

Launch discipline

For off-plan, prioritise tier-1 developers, construction progress, escrow discipline, and delivery track record. Be wary of over-amenitised, high-service-charge stock marketed on glossy yields.

Yield guardrails (quick rules of thumb)

Aim for net 5–6% on prime cores, 6.5–7.5% on mid-market. Stress-test at +100 bps cap-rate and –10% rent; avoid deals that break covenants under that.

H1 2025 Community Breakdown: Apartments vs Villas:

While complete community-level splits (units, value, yields) aren’t published in a single source, we can build a clear picture using available data:

Overall performance (H1 2025):

Apartment units sold: 73,863 – Up 15% vs H1 2024.

Total sales volume: +22.5%; sales value: +40.1% YoY.

Jumeirah Village Circle, Business Bay, and Dubai Production City were leading hubs in the off-plan space.

Downtown Dubai apartments: average sales price AED 4.31M; ROI 5.68%

Trends to note:

Apartments dominate in volume, driven by off-plan activity in mid-market corridors.

Villas, especially luxury, fetch premium pricing and appeal to long-term and high-net-worth buyers, but yield slightly lower.

Resale/home-ready units are gaining traction alongside off-plan, moderating dynamics between segmented market tiers

Handover & Supply Timeline: H2-2025 and Into 2026

H1 2025 Completions & Pipeline:

Units completed: 17,300

Units under construction: 61,800; projected for 2026–27: 100k+

New unit registrations in H1: 90,337; projected 150,000 by year-end; 250k across 2023–2026, with peak deliveries in 2026 (120k)

2025–2026 Supply Surge:

An estimated 41,000 and 42,000 planned completions are expected in 2025 and 2026, respectively.

Fitch projects up to a 15% decline in prices during H2 2025 into 2026 due to a supply glut, though prime areas may soften less.

Specific Handovers & Development Trends:

High-profile handovers are scheduled, for example, at Creek Crescent and Emaar Beachfront Residences.

Notable recent handover: Westwood Grande II in JVC, 153 units delivered in May 2025.

Handover delays are common, affecting 62% of scheduled 2025 projects, and this rate further drops to around 48% in 2026 due to supply chain and logistical pressures.

Summary: What This Means (H2 2025 → 2026)

– Apartment (off-plan mid-market corridors): Expect heightened post-handover supply pressure; developers could lean into incentives and discounts to absorb inventory. Expect moderation in price growth.

– Prime apartments (Marina, Downtown, Palm): Resilient, but likely slower growth, still a yield haven for investors. Some projects are fundamentally undervalued, though this is more prevalent in the ultra-luxury sector in Dubai. For instance, Six Senses Palm Jumeriah is now trading over 100% ROI, still Off-Plan, from its OP.

– Villas (luxury enclaves): Less supply-sensitive inertia; expectations for continued demand from UHNW and speculative investors.

– Rental market: Slight rent softening, especially in studios/1-beds, as new supply gives tenants leverage; villa rents stay firmer due to scarcity.

– Risk factors: Mistimed off-plan exposure (without a clear delivery schedule), over-entering mid-market stock without leasing flow, and reliance on price momentum.

Off Plan Dubai helps investors enter the UAE property market every month; some invest from afar, while others live closer to the action. Some plan on moving immediately, while others plan to move in the near or distant future. Some never.

However, a primary consideration is how the schools in the UAE compare to those in other regions, as well as the associated costs.

I’ve put an interactive table on your screen showing indicative annual tuition ranges by curriculum and stage for 2025/26 (FS1/Pre-K, Year 6/Grade 5, Year 10/Grade 9, Year 13/Grade 12). The ranges come from GEMS’ network fee guide and line up well with what you’ll see across the market. We refer to KHDA throughout the post: Knowledge and Human Development Authority.

What the ranges look like (2025/26)

British: roughly AED 8.7k – 98.5k from FS1 to Year 13.

IB/American: roughly AED 23k – 117.6k from FS1/PK to Grade 12 (IB years skew high at DP level).

Indian (CBSE/ICSE): roughly AED 9.8k – 54k from KG to Grade 12 (widest value spread; strong “good/very good” options at lower fees).

Concrete examples (to anchor the ranges):

Deira International School (British/IB, Outstanding): AED 44,616 (FS1) to AED 89,889 (Year 13), 2025/26.

Dubai English Speaking College (British): AED 84,326 (Y7–Y11) and AED 90,633 (Sixth Form).

Dubai British School – Jumeirah Park (British): AED 64,160 (Y1) to AED 83,015 (Y13).

KHDA directory links every school’s official “School Fees Fact Sheet” (one-page, all charges listed). Use this to confirm any school’s exact line-items before enrolling.

2025/26 fee movement (why some numbers nudged up)

For 2025–26, KHDA set the Education Cost Index (ECI) at 2.35%, which is the cap many for-profit schools can apply for fee increases this year. Expect most “premium” schools to have moved modestly within that cap.

What adds to tuition (and where to check):

Besides base tuition, families typically face:

Application/registration (often ~AED 500), transport, uniforms, books, technology, exam fees (IGCSE/IB/A-level), activities/trips, and sometimes SEN/EAL support. All of these must appear on the KHDA School Fees Fact Sheet—use that document as the single source of truth.

How to choose by value (quick heuristics):

First, consider curriculum fit (UK vs IB vs US vs Indian); then compare KHDA ratings and outcomes (GCSE/IB results) per dirham of tuition.

For substantial value at lower fees, short-list Indian curriculum schools or “good/very good” UK schools; for IB DP or UK Sixth-Form excellence, budget for the upper bands. Use the KHDA directory to scan ratings and open each school’s Fees Fact Sheet directly.

In Dubai, location has a significant impact on the fees of the school you wish to attend.

Location in Dubai really does influence school fees—not just because of which schools are nearby, but also due to catchment zones, local demand, and perceived prestige. Let’s compare Emirates Hills and Dubai Hills Estate area schools to give you a clearer picture:

Emirates Hills

Dubai International Academy (DIA), Emirates Hills

Curriculum: IB (KG1–Year 13)

Annual tuition: AED 42,832–77,866 per year for 2024–25; average around AED 59,500

External sources estimate fees for Year 1–Year 13 between AED 53,027–79,541 (2025/26)

Other nearby options

Emirates International School, Meadows (IB): around AED 27,000–74,000 annually, depending on age group

Summary (Emirates Hills corridor):

IB schools (e.g., DIA): AED 43k–78k

British schools (e.g., DBS): AED 52k–78k+

Schools nearby with Indian/IB options: a mix ranging from AED 27k to 74k, adding value for perhaps more modest fees.

Dubai Hills Estate Area

This area doesn’t host large international schools, yet, like Emirates Hills, but it’s proximate to several Indian-curriculum and value-focused schools.

GEMS New Millennium School, Dubai Hills Estate

Curriculum: British & Indian (all-through)

Annual tuition: approx. AED 27,000

Rating: “Very Good” by KHDA

Other Indian schools nearby:

Springdales School (Al Quoz): AED 26,500 (Good)

Dewvale School (Al Quoz): AED 15,000 (newer school)

These schools are more budget-friendly, especially for families leaning toward the Indian curriculum.

Key Takeaways:

Prestige & curriculum drive higher fees—Emirates Hills is home to top-rated “Outstanding” IB and British schools mid-to-high in the AED 40k–80k range.

Dubai Hills Estate offers excellent value—particularly with Indian/British curriculum options under AED 30k, though KHDA ratings may range from Good to Very Good.

No one-size-fits-all—if budget is a priority and an Indian curriculum is acceptable, Dubai Hills may suit. But for award-winning IB/British education and premium facilities, Emirates Hills commands a premium.

I hope everyone is doing well. I am currently sitting in the heart of Mayfair in a coffee shop, typing this, and looking forward to the launch of Fahid Island today. Many astute, long-term investors are about to purchase a future icon in Abu Dhabi real estate at the very initial launch prices. This is fundamental to our recommendations and role.

Last week, Fitch Ratings Agency predicted a 15% market correction in the Dubai market in late 2025 that will continue into the early stages of 2026. For those who speak to me regularly, we have been predicting this for the last 8/12 months. As someone who has been in the market for over a decade, I wanted to give my thoughts on how it would benefit the market and help investors in the long term.

Fundamentally, I believe in the market now and in the future. Investments now more than ever have to have a mid/long-term play, but if you buy in the correct location, from the right developer at the right price, you will see opportunities a-plenty over the coming years.

The Forecast

Prices could dip 10-15% in the next 18 months.

Why? Oversupply 250,000 Units launched in 203-24 with 120,000 units scheduled for handover in 2026.

Population Growth stands at 5% per year.

Too many apartments mean Rental Yields will slip as the supply hits the market, causing weaker areas and over-leveraged developers to hit the market.

What does this mean?

Prime Villas / Prime Masterplans and Quality Developers – likely safe

Speculative Apartment Zones – Real Risk Ahead If Fitch is cautious, banks and lenders will start to be, too. Over-leveraged developers will become susceptible to these market fluctuations.

15%?

If 15% is the maximum figure, the market would be at levels seen in early 2024. Those who have invested in the market for extended periods would remember 2008 and pre-COVID market dynamics. Think long-term, buy what lasts for families once the buying hype fades.

Opportunites

If you have been looking at a ready property, in the next year or so, you will find the prices at which you may be more willing to transact. Many investors will see opportunities, and the number of transactions may increase as people ‘buy the dip’.

Developers improve payment plans. If off-plan transactions stabilise, developers will offer better payment terms to entice buyers. This will be minimal in prime locations, but if you like to purchase with speculative developers in a risk range portfolio, you will see offers that may attract.

How to navigate?

We pride ourselves on promoting projects, developers, and master plans we believe in. I say no more than I would ever say yes when investors ask for advice. No one can ever accurately predict the future, but there are principles I adhere to that help us best avoid any market issues.

Developer – Always pick a government-backed developer or an extremely cash-rich private one. Aldar / Emaar – Government Backed. DAR Global / Select / Omniyat – Publicly listed cash-rich developers. These developers don’t need your installment payments to complete builds. You could get real development issues if you get a % of over-leveraged off-plan investors within one particular project.

Masterplan—The best developers don’t build individual Tower Blocks or 30 Villas in the desert. They harbour communities and facilities that emphasise the standard of living and the finished project. In the right master plan, the whole community drives appreciation. What schools, medical, and other facilities are being built where you invest?

Master plans that will outperform others and be less susceptible to market fluctuations:

Polo Oasis Dubai Hills Estate Beachfront Fahid Island Yas Island Athlon DIFC Dubai Islands

Location—Recently, you have seen that we have shifted into the Abu Dhabi market more prominently. Aldar will be one of the most important developers in the GCC over the next 10 years. Abu Dhabi is targeting HNW families, and the Villa launches are some of the best you will see anywhere in the world. It is less busy and family-oriented, and you will see a conscious shift in buying habits from Dubai to Abu Dhabi. We believe in diverse portfolios, whether unit type or location, which is why you see us covering areas such as London, Manchester, Riyadh, Jeddah, Oman, Qatar, and Marbella, among others.

Entry Price – Your purchasing price per sqft matters most at the entry point. When buying off-plan, you should look at a project that is around 30-40% below market value if that product is ready in the completed master plan. This week’s recent transaction in Six Senses Palm, a two-bedroom, was exchanged above the 20m AED mark for the first time. It was initially purchased for 12m and has now been sold 3 times during construction. If the original investor had kept the unit, the returns on Capital from the 60/40 payment plan would now surpass 100%. When launched, some investors would think that 12m for a 2-bedroom apartment was expensive. But it had the correct location, a leading brand behind it, and comparables in the vicinity showed it was vastly under-valued compared to if it were ready.

Industry – Speaking candidly, the level of Real Estate employees working in the Dubai Real Estate market isn’t of an industry-leading standard. They chase quick wins for quick paydays. In the last 4 years, anyone can sell in this market; it sells itself. When the market turns a couple of %, you will see agents calling you, telling you to sell now before you lose more money, creating a false panic, and them wanting a commission when the correct advice may be completely different, but it doesn’t benefit their pocket.

Agents don’t take a basic wage from 99% of the real estate agencies, and their tactic has always been to throw enough s**t at a wall, and some will stick.

Every other person in Dubai seems to be a property expert and a current agent. I look forward to the market becoming difficult and true advice and expertise being valued again. Over the coming years, you will see most agents flushed out of the ecosystem and a smaller, well-informed collection of agents still trading.

Honesty & Integrity

I hope you can see that no matter what happens in the future, our advice comes from a place of integrity, market knowledge, and above all, honesty.

Play mid/long term, embrace the whole journey, and if you believe fundamentally in the market and region, as I do, a market correction can provide opportunities and risk simultaneously. Enjoy the highs, embrace and plan for the lows.

Get in touch

Dubai Office

Off Plan Dubai

Suite: 508, Fairmont, Sheikh Zayed Road, P O Box 75671, Dubai, UAE