Saudi Arabia continues to push the boundaries across multiple sectors, and none more so than the Real Estate Sector. Off Plan Dubai, now in just over 18 months, has transacted over 500m SAR of real estate with HNWI investors, Family/Private offices, and this rapid growth shows no signs of slowing down.

We have now been operational and profitable for over 10 years, initially focusing solely on Dubai, and we have since added London and Manchester to our investment portfolio offerings. The UK has some of the tightest regulations seen anywhere in the world. Following the 2008 market crash, RERA revamped many aspects of the Real Estate process in Dubai, and as such, investors are much more protected than they were previously.

Saudi Arabia, driven by multi-layered growth, emerged as a market we aimed to target comprehensively. Our investors sought diverse options, and we sought to accelerate our growth and establish ourselves as a leading international player in the Real Estate sector.

Our primary concern was investor protection and the regulations that safeguard investor capital. We conducted a thorough review of the process, and the primary protection framework is outlined in the WAFI agreement. Here is a concise summary of how it works and how it compares to the REAR regulations in Dubai.

The Wafi program is Saudi Arabia’s regulatory framework governing the sale and marketing of off-plan real estate projects. Administered by the Ministry of Municipal and Rural Affairs and Housing, it ensures that developers cannot simply launch and sell projects without meeting strict licensing and financial conditions. To secure approval, a developer must present detailed project plans, economic feasibility studies, and secure guarantees, with all customer payments deposited into a dedicated, regulated Escrow Account. These funds can only be released in line with verified construction progress, preventing misuse of investor money and reducing the risk of incomplete developments.

For investors, this means that when they sign a Wafi Agreement, they are legally protected: developers are monitored, construction progress is independently reviewed, and buyers’ funds are safeguarded. This framework aligns Saudi Arabia with global standards, similar to escrow systems used in Dubai, and reflects the government’s aim to build trust and transparency in the off-plan market. By requiring financial discipline and strict oversight, WAFI helps ensure that investors are not just buying into promises, but into regulated, deliverable projects. As an advisory, we always aim to work with projects where payments on the payment plan are construction-linked. Only once the independent surveyor has verified a construction milestone can a payment request be initiated.

Here’s a clear side-by-side comparison of Saudi Arabia’s WAFI system and Dubai’s RERA escrow law, tailored for investors considering off-plan property:

WAFI (Saudi Arabia) vs RERA Escrow (Dubai)

1. Regulatory Body

WAFI (Saudi): Managed by the Ministry of Municipal and Rural Affairs & Housing.

RERA Escrow (Dubai): Overseen by the Real Estate Regulatory Authority (RERA) under the Dubai Land Department.

2. Developer Requirements

WAFI: Developers must obtain a WAFI license, provide feasibility studies, and meet strict financial guarantees before selling.

RERA: Developers must register projects with RERA, open a project-specific escrow account, and submit financial guarantees.

3. Buyer Payment Protection

WAFI: All buyer payments go into a regulated escrow account; funds are released only after verified construction progress.

RERA: Payments are also held in escrow and released to developers according to construction milestones confirmed by independent auditors.

4. Oversight & Monitoring

WAFI: Regular audits, inspections, and progress checks by licensed engineers appointed by the ministry.

RERA: Continuous monitoring with mandatory developer reporting and independent audit verification.

5. Penalties for Non-Compliance

WAFI: Developers face fines, license suspension, and potential blacklisting from future projects.

RERA: Heavy fines, cancellation of projects, and restrictions on developer activities.

6. Investor Confidence

WAFI: A relatively newer system (introduced mid-2010s) but increasingly robust, designed to protect buyers and attract foreign investment.

RERA: Established in 2007 and globally recognised, it provides a strong track record that has built international trust in Dubai’s off-plan market and has vastly improved since the 2008 Market Crash.

Key takeaway for investors: Both systems aim to safeguard buyer funds and ensure delivery, but Dubai’s RERA is more mature and time-tested. At the same time, Saudi Arabia’s WAFI is newer but backed by substantial government reforms under Vision 2030. This positions Saudi off-plan as an emerging, regulated market with increasing protections, similar to Dubai a decade ago.

At Off Plan Dubai, for over 10 years, we have assisted investors, offices and funds in placing capital into some of the most lucrative Off Plan Investments in Dubai and, more recently, other international markets. Our business is now built on referrals and repeat business, which requires a significant level of trust. Ultimately, this means our investors achieve significant Capital Appreciation on the investments they make.

We do this on numerous fronts, and we mean test all investments across a set of fundamentals that you can measure within the market. Firstly, it is essential to understand that Dubai’s property appreciation isn’t random; it tends to follow specific economic, demographic, and policy-driven cycles. We obviously hope you choose to partner with Off Plan Dubai for any future property purchase, but if you wish to understand our process yourself, here are the most impactful factors that cause property values in Dubai to rise, and whether they’re monitorable and predictable:

Key Drivers of Property Appreciation in Dubai:

Population Growth & Inflow of Residents

Dubai’s real estate values rise when population inflows (expats, high-net-worth individuals, new residents through Golden Visas) outpace new supply.

Monitorable? Yes — population growth, visa issuances, and migration trends are reported by the Dubai Statistics Centre and immigration authorities. One of our key population metrics is to calculate the annual number of new residents compared to the number of Off Plan Units sold. For instance, Abu Dhabi currently has 19 new residents for every unit sold.

Supply & Demand Balance

Oversupply has historically slowed appreciation (e.g., 2015–2019), while controlled launches (as seen post-2021) push prices up. In some regions of Dubai, we are currently monitoring a trend of over-launching, which is more prevalent in Master-plans where developers can buy individual plots rather than being fully managed by one leading Master Developer.

Monitorable? ✅ Yes – compare project launches with handovers via DLD (Dubai Land Department) and major consultancies (Knight Frank, CBRE, JLL).

Government Policies & Regulations

Examples: Golden Visa, 100% foreign ownership of companies, retirement visa, and foreign investment reforms. Each policy wave historically boosted demand and prices. These are cross-demographic and impact multiple nationalities.

Monitorable? ✅ Yes – policy announcements are public and often give a lead indicator of demand surges.

Infrastructure & Mega Projects

Big-ticket projects (Palm Jumeirah, Dubai Hills Estate, Rashid Yachts & Marina, Dubai Creek Harbour, Palm Jebel Ali) create long-term appreciation around those zones.

Monitorable? ✅ Yes – Track announced government infrastructure plans and developer masterplans. Examples include extensions of metro lines and multi-million/billion logistics improvements, as seen recently at the entry and exit of Emaar Beachfront, which serves as a strong example.

Interest Rates & Global Liquidity

The UAE dirham is pegged to the USD, so Fed rate cuts/raises directly impact mortgage affordability and investor appetite. The saying goes that the US sneezes and the world catches a cold; this is even more relevant to the UAE, who are pegged against the currency.

Monitorable? ✅ Yes — follow US Fed policy and UAE Central Bank rate moves.

Investor Sentiment & Global Capital Flows

Dubai attracts inflows when there’s instability elsewhere (Russia-Ukraine, high taxation in Europe, currency devaluation in Asia). Dubai is exceptional at proving to be a haven when turmoil hits other regions. A super strong, decisive leadership, as seen through COVID-19, and a low-tax, tax-free society that rewards entrepreneurs and innovators, the world’s talent sees the UAE and Dubai as a hotspot to flourish.

Monitorable? ⚠️ Partially — geopolitical shocks are unpredictable, but you can track capital flow trends and residency program demand. Although slightly morbid in nature, Dubai is often viewed as a highly safe destination for both the populace and capital in the event of any political conflict or, god-forbid, war.

Tourism & Economic Growth

Dubai’s property cycle aligns with its success as a tourism, trade, and financial hub. More businesses and visitors = higher housing demand.

Monitorable? ✅ Yes – Dubai Tourism (DTCM) stats and GDP growth projections.

Limited Land in Prime Zones

Areas like Palm Jumeirah, Downtown, Jumeirah Bay, and Dubai Hills have scarcity value, creating outsized appreciation compared to emerging zones.

Monitorable? ✅ Yes – supply pipeline shows where scarcity will persist.

Can We Predict Appreciation?

Short-term (1–2 years): Yes, by watching supply handovers, Fed rate policy, and government reforms.

Medium-term (3–5 years): Trends can be modelled based on population inflow vs. supply, but shocks (COVID, oil prices, geopolitics) can change trajectories.

Long-term (10+ years): More predictable in prime and master-planned zones (Palm, Dubai Hills, Creek Harbour) where infrastructure and limited land sustain demand.

Investor Takeaway:

To anticipate appreciation, you want to track three leading indicators consistently:

Supply vs. demand pipeline → handovers vs. visa/population growth.

Global interest rates & liquidity → mortgage and investor flows.

We monitor the above monthly and quarterly, and evaluate the numbers annually. Here is our framework that we send to our investors. For some individual projects, we can identify undervalued projects by comparing the price per sqft at launch to real-life comparables. We like to incorporate this process into the framework below.

Dubai Property Appreciation Watchlist Framework:

1. Demand-Side Indicators Why it matters: Rising demand without equivalent supply = appreciation.

Population growth & new visas issued.

Sources: Dubai Statistics Centre, GDRFA, press releases on Golden Visa/Residency Visa uptake.

What to watch: Quarterly inflow of new residents; high spikes indicate demand surges.

Foreign direct investment in real estate

Sources: Dubai Land Department (DLD) reports, Knight Frank, CBRE.

What to watch: Nationalities leading purchases (e.g., Russians 2022–23, Indians, Chinese, Europeans).

Tourism numbers

Sources: DTCM reports.

What to watch: Hotel occupancy & visitor count (short-term rental demand).

Quarterly: Review population inflows, tourism data, and handover vs. launch balance.

Annually: Assess mega-project completions, supply pipeline, and global capital inflows.

The Dubai market has provided opportunities since COVID that have literally changed people’s financial lives. Investors are now naturally wondering if the opportunity has passed them by or if there are still opportunities and potential to make solid money over the coming years. We have gone through the first half of the year, and here is a clean, data-driven read on H1-2025 and what it signals for H2-2025 into 2026.

Where transactions were heaviest (H1-2025)

Top areas by number of deals (DLD data):

Al Barsha South Fourth – 10,469

Al Yalayis 1 – 7,595

Wadi Al Safa 5 – 7,178

Next tier included Business Bay (6,601), Dubai Marina (6,428), Airport City (5,569), Jebel Ali First, Al Thanyah Fifth, Burj Khalifa (Downtown), Meaisem First.

Top areas by value (H1-2025):

Dubai Marina – AED 25.1bn

Business Bay – AED 22.5bn

Burj Khalifa (Downtown Dubai) – AED 17.1bn

Palm Jumeirah – AED 16.96bn (also high: Al Yalayis 1, Meaisem Second, Wadi Al Safa 5, Airport City, Al Barsha South Fourth).

Big H1-2025 market signals (headline numbers):

Record half-year: total real-estate procedures exceeded AED 431bn, with circa 99k sales and strong investor participation.

Off-plan continued to lead the way (circa 65%+ share by count) with apartments accounting for 80% of deals; meanwhile, secondary gained momentum.

Price growth is still positive (values up ~14% y/y to June), but it is more segmented by community.

Supply pressure: 20k+ units delivered in H1, with a large handover wave expected in H2; pipeline 200k+ through 2027. Completions concentrated in JVC, Sobha Hartland, and MBR City. We have continued to speak about trepidation in areas with high concentrations of handovers.

DXBinteract mid-year: transactions +22.5% y/y by count, +40% by value; mortgages up by volume but lower average ticket, more cash but placed on smaller loans.

Hot Locations:

Value magnets: Marina, Business Bay, Downtown/Burj Khalifa, Palm — luxury/brand-led stock, investor depth, and liquidity; these continue to set the pace for AED value.

Volume workhorses: Al Barsha South Fourth, Al Yalayis 1, Wadi Al Safa 5 — areas with heavy off-plan launches and mid-market price points (broad buyer pools, investor-friendly ticket sizes). At Off Plan Dubai, we do not cover these areas, but appreciate the ‘bulk’ of the market they provide.

Affordable/mid-market momentum: JVC/Arjan/Dubailand corridors saw big handovers and sales churn; this is where any supply-driven price moderation shows up first.

What to watch out for in H2-2025 → 2026

1) Supply digestion vs. price growth

The handover bulge in H2 (after 20k+ in H1) should cool quarterly price growth for mid-market apartments in outer corridors; expect more competitive pricing & incentives from developers. Prime/luxury remains more resilient but likely slower growth off a higher base.

2) Off-plan still dominant, but resale continues its race to catch up:

DXBinteract shows secondary prices rising faster y/y than off-plan in several segments; that can keep ready units in mature family communities (e.g., Dubai Hills, Arabian Ranches, Jumeirah Park) in demand. DXB Interact

3) Financing mix

Mortgage counts up, values down → more cash buyers/smaller LTVs. If rates ease into 2026, you could see resale liquidity improve and upgrade activity pick up.

4) Infrastructure catalysts

DWC/Al Maktoum Airport expansion and Dubai South narrative continue to build; land/early-phase townhouse projects there should see sustained enquiry.

5) Leasing

Rent growth moderating from 2023–24 highs as supply lands, especially in studios/1-beds; villa rents remain stickier due to scarcer stock. (

Strategy for an investor (actionable):

Hold/accumulate in value-dense, liquid cores (Marina, Business Bay, Downtown micro-units with strong STR/long-let demand) for AED value preservation and exit liquidity.

Selective growth in outer mid-market (JVC/Al Barsha South Fourth/Wadi Al Safa 5) after handover waves. Negotiate on post-handover inventory, focus on buildings with proven leasing velocity and realistic service charges.

We have a strong preference for the Villa market, focusing on areas like Polo and The Valley by Emaar.

Resale family villas/townhouses

Target ready units in established school-adjacent communities; these held pricing better in H1 and should remain bid if rates ease in 2026.

Launch discipline

For off-plan, prioritise tier-1 developers, construction progress, escrow discipline, and delivery track record. Be wary of over-amenitised, high-service-charge stock marketed on glossy yields.

Yield guardrails (quick rules of thumb)

Aim for net 5–6% on prime cores, 6.5–7.5% on mid-market. Stress-test at +100 bps cap-rate and –10% rent; avoid deals that break covenants under that.

H1 2025 Community Breakdown: Apartments vs Villas:

While complete community-level splits (units, value, yields) aren’t published in a single source, we can build a clear picture using available data:

Overall performance (H1 2025):

Apartment units sold: 73,863 – Up 15% vs H1 2024.

Total sales volume: +22.5%; sales value: +40.1% YoY.

Jumeirah Village Circle, Business Bay, and Dubai Production City were leading hubs in the off-plan space.

Downtown Dubai apartments: average sales price AED 4.31M; ROI 5.68%

Trends to note:

Apartments dominate in volume, driven by off-plan activity in mid-market corridors.

Villas, especially luxury, fetch premium pricing and appeal to long-term and high-net-worth buyers, but yield slightly lower.

Resale/home-ready units are gaining traction alongside off-plan, moderating dynamics between segmented market tiers

Handover & Supply Timeline: H2-2025 and Into 2026

H1 2025 Completions & Pipeline:

Units completed: 17,300

Units under construction: 61,800; projected for 2026–27: 100k+

New unit registrations in H1: 90,337; projected 150,000 by year-end; 250k across 2023–2026, with peak deliveries in 2026 (120k)

2025–2026 Supply Surge:

An estimated 41,000 and 42,000 planned completions are expected in 2025 and 2026, respectively.

Fitch projects up to a 15% decline in prices during H2 2025 into 2026 due to a supply glut, though prime areas may soften less.

Specific Handovers & Development Trends:

High-profile handovers are scheduled, for example, at Creek Crescent and Emaar Beachfront Residences.

Notable recent handover: Westwood Grande II in JVC, 153 units delivered in May 2025.

Handover delays are common, affecting 62% of scheduled 2025 projects, and this rate further drops to around 48% in 2026 due to supply chain and logistical pressures.

Summary: What This Means (H2 2025 → 2026)

– Apartment (off-plan mid-market corridors): Expect heightened post-handover supply pressure; developers could lean into incentives and discounts to absorb inventory. Expect moderation in price growth.

– Prime apartments (Marina, Downtown, Palm): Resilient, but likely slower growth, still a yield haven for investors. Some projects are fundamentally undervalued, though this is more prevalent in the ultra-luxury sector in Dubai. For instance, Six Senses Palm Jumeriah is now trading over 100% ROI, still Off-Plan, from its OP.

– Villas (luxury enclaves): Less supply-sensitive inertia; expectations for continued demand from UHNW and speculative investors.

– Rental market: Slight rent softening, especially in studios/1-beds, as new supply gives tenants leverage; villa rents stay firmer due to scarcity.

– Risk factors: Mistimed off-plan exposure (without a clear delivery schedule), over-entering mid-market stock without leasing flow, and reliance on price momentum.

Off Plan Dubai helps investors enter the UAE property market every month; some invest from afar, while others live closer to the action. Some plan on moving immediately, while others plan to move in the near or distant future. Some never.

However, a primary consideration is how the schools in the UAE compare to those in other regions, as well as the associated costs.

I’ve put an interactive table on your screen showing indicative annual tuition ranges by curriculum and stage for 2025/26 (FS1/Pre-K, Year 6/Grade 5, Year 10/Grade 9, Year 13/Grade 12). The ranges come from GEMS’ network fee guide and line up well with what you’ll see across the market. We refer to KHDA throughout the post: Knowledge and Human Development Authority.

What the ranges look like (2025/26)

British: roughly AED 8.7k – 98.5k from FS1 to Year 13.

IB/American: roughly AED 23k – 117.6k from FS1/PK to Grade 12 (IB years skew high at DP level).

Indian (CBSE/ICSE): roughly AED 9.8k – 54k from KG to Grade 12 (widest value spread; strong “good/very good” options at lower fees).

Concrete examples (to anchor the ranges):

Deira International School (British/IB, Outstanding): AED 44,616 (FS1) to AED 89,889 (Year 13), 2025/26.

Dubai English Speaking College (British): AED 84,326 (Y7–Y11) and AED 90,633 (Sixth Form).

Dubai British School – Jumeirah Park (British): AED 64,160 (Y1) to AED 83,015 (Y13).

KHDA directory links every school’s official “School Fees Fact Sheet” (one-page, all charges listed). Use this to confirm any school’s exact line-items before enrolling.

2025/26 fee movement (why some numbers nudged up)

For 2025–26, KHDA set the Education Cost Index (ECI) at 2.35%, which is the cap many for-profit schools can apply for fee increases this year. Expect most “premium” schools to have moved modestly within that cap.

What adds to tuition (and where to check):

Besides base tuition, families typically face:

Application/registration (often ~AED 500), transport, uniforms, books, technology, exam fees (IGCSE/IB/A-level), activities/trips, and sometimes SEN/EAL support. All of these must appear on the KHDA School Fees Fact Sheet—use that document as the single source of truth.

How to choose by value (quick heuristics):

First, consider curriculum fit (UK vs IB vs US vs Indian); then compare KHDA ratings and outcomes (GCSE/IB results) per dirham of tuition.

For substantial value at lower fees, short-list Indian curriculum schools or “good/very good” UK schools; for IB DP or UK Sixth-Form excellence, budget for the upper bands. Use the KHDA directory to scan ratings and open each school’s Fees Fact Sheet directly.

In Dubai, location has a significant impact on the fees of the school you wish to attend.

Location in Dubai really does influence school fees—not just because of which schools are nearby, but also due to catchment zones, local demand, and perceived prestige. Let’s compare Emirates Hills and Dubai Hills Estate area schools to give you a clearer picture:

Emirates Hills

Dubai International Academy (DIA), Emirates Hills

Curriculum: IB (KG1–Year 13)

Annual tuition: AED 42,832–77,866 per year for 2024–25; average around AED 59,500

External sources estimate fees for Year 1–Year 13 between AED 53,027–79,541 (2025/26)

Other nearby options

Emirates International School, Meadows (IB): around AED 27,000–74,000 annually, depending on age group

Summary (Emirates Hills corridor):

IB schools (e.g., DIA): AED 43k–78k

British schools (e.g., DBS): AED 52k–78k+

Schools nearby with Indian/IB options: a mix ranging from AED 27k to 74k, adding value for perhaps more modest fees.

Dubai Hills Estate Area

This area doesn’t host large international schools, yet, like Emirates Hills, but it’s proximate to several Indian-curriculum and value-focused schools.

GEMS New Millennium School, Dubai Hills Estate

Curriculum: British & Indian (all-through)

Annual tuition: approx. AED 27,000

Rating: “Very Good” by KHDA

Other Indian schools nearby:

Springdales School (Al Quoz): AED 26,500 (Good)

Dewvale School (Al Quoz): AED 15,000 (newer school)

These schools are more budget-friendly, especially for families leaning toward the Indian curriculum.

Key Takeaways:

Prestige & curriculum drive higher fees—Emirates Hills is home to top-rated “Outstanding” IB and British schools mid-to-high in the AED 40k–80k range.

Dubai Hills Estate offers excellent value—particularly with Indian/British curriculum options under AED 30k, though KHDA ratings may range from Good to Very Good.

No one-size-fits-all—if budget is a priority and an Indian curriculum is acceptable, Dubai Hills may suit. But for award-winning IB/British education and premium facilities, Emirates Hills commands a premium.

Off-Plan Dubai from 2024 onwards firmly established itself as a leading player in the Saudi real estate landscape. We have partnered with local funds and developers to invest in the Kingdom through real estate, and we have witnessed the region’s growth in prominence across multiple continents as the world’s smart money moves there in anticipation of the upcoming boom in the real estate sector. We are fast approaching SAR 500m in just under 2 years in the market, that’s not in any way a gloat or showing off. Just a validation that we know the region and investment sector, and are continuing to provide value and insights into an internationally emerging investment destination.

If you’re considering investing in Riyadh real estate, here’s a well-rounded look at the current landscape as of mid-2025:

Why Riyadh Is Attracting Investor Interest:

Vision 2030 and Major Development Projects: Riyadh sits at the center of Saudi Arabia’s Vision 2030, an ambitious plan to diversify the economy beyond oil. This includes massive infrastructure and urban development initiatives that buoy real estate demand.

Key mega-projects include:

Riyadh Metro: operational since December 2024, provides critical connectivity across the city.

New Murabba: a futuristic downtown featuring the Mukaab skyscraper, is set for completion by 2030.

King Salman Park: on track to be one of the world’s largest urban parks, is opening in 2026.

King Abdullah Financial District: (KAFD) is a LEED-Platinum mixed-use district catering to businesses and residents.

Strong Market Performance & Growth Trends:

Residential and commercial sectors are seeing heightened activity:

A 38% jump in real estate transactions in H1 2024, totalling SAR 127.3 billion. CBRE reports an 18% rise in average rents for office spaces in 2024, with Q1 2025 showing a 21% year-on-year jump, driven by limited available space.

Property values climbed by 5.1% in Q1 2025.

Market forecasts remain positive:

JLL anticipates the real estate market’s value to hit $101.6 billion by 2029, with an 8% compound annual growth rate from 2024.

Crown Continental projects rental yields of 8.5%–9.5% in 2025, property price growth of 3%–7%, and capital appreciation of 4%–8%.

The residential sector remains robust, and hospitality, retail, and logistics are expanding as well.

Foreign Investment & Ownership Reforms:

Since 2023, foreigners can now own freehold real estate in many parts of Riyadh, including residential, commercial, and mixed-use projects.

Other incentives include relaxed ownership rules, long-term residency “Green Card” options, and streamlined regulations.

Net FDI in Q4 2024 rose by 26%, with projections calling for $100 billion in FDI by 2030.

Legal Reform & Key Timelines:

Starting January 2026, Saudi Arabia will dramatically open its real estate market to foreign ownership—under a finely regulated, zone-based system. This represents a historic shift, enabling international investors, expats, and global firms to participate in the Kingdom’s real estate economy while maintaining protective controls. Legal guidance, awareness of zone-specific rules, and careful compliance will be essential as the policy rolls out.

On July 25, 2025, Saudi Arabia officially published a groundbreaking law—the Law of Real Estate Ownership and Investment by Non-Saudis—replacing the earlier 2000 framework.

The law enters into force 180 days after publication, which places its effective date in January 2026.

Detailed executive regulations defining eligible zones, ownership limits, procedures, and enforcement mechanisms will be published within that 180-day transition period.

Saudi Arabia – Premium Residency (Green Card) Real Estate Investment Visa:

Eligibility Requirements:

Property Value: Own (or hold usufruct rights to) a residential property in Saudi Arabia valued at ≥ SAR 4 million (~USD 1.07 million).

No Financing Allowed: The property must be fully developed, mortgage-free, and not financed at any point—meaning purchase must be made in cash without leverage.

Valuation: It must be appraised by a valuator accredited by the Saudi Authority for Accredited Valuers (Taqeem).

Residency Duration: The residency remains valid as long as you retain ownership of the qualifying property or usufruct rights over it.

Fees: A one-time government fee of SAR 4,000 (~USD 1,066), plus a processing fee (often around USD 170), is required for the application.

Benefits Include:

Reside in Saudi Arabia with your family, including spouses, children under 25, and even parents.

Visa-free exit and re-entry, and exemptions from expat and dependent fees. Work and change employers freely in the private sector without needing a local sponsor.

Own real estate, vehicles, and businesses, and invite relatives via visit visas.

Use dedicated lanes at airports for faster processing.

Key Risks and Challenges to Be Aware Of:

Off Plan Dubai, as with all investments, especially emerging markets, it is essential to consider any potential pitfalls and obstacles that may present themselves. If we are aware of upcoming issues, we can best plan for them and mitigate them as effectively as possible.

Regulatory and bureaucratic hurdles: Despite reforms, navigating local bureaucracy can be slow and complex, particularly for foreign investors. In truth, this is why we like working with multi-national developers. They have a process that has been fine-tuned across multiple markets and makes international investing as easy as possible.

Value volatility: Property values remain tied to broader economic factors, notably oil prices. Saudi Arabia is aiming to thrive beyond the notion of oil dependency and become a functioning state in its own right.

High prices and affordability issues: Since the pandemic, prices have surged—home prices up 81%, apartments 56%, making ownership increasingly out of reach for many locals.

White land tax initiative: A new tax (up to 10%) on underdeveloped land aims to curb speculation and encourage development, which may affect investment strategies in undeveloped zones.

Rental inflation concerns: Anecdotal reports highlight rapid rent hikes, even for older properties. North Riyadh has experienced unprecedented annual jumps from SAR 12,000 to SAR 70,000, despite poor conditions in some buildings.

Prime Investment Areas & Property Types

Promising neighbourhoods for investment (especially for residential, rental, or Airbnb-style units):

Al Malqa: Upscale villas, well-located.

Sedra: Home to DAR Global and Roshn Luxury Villas, all centred around a natural Wadi. A crown in Riyadh Real Estate.

Al Narjis, Al Yasmin: Family-friendly with strong rental demand.

Al Narjis & Jasmine: Popular with upper-middle-class segments.

KAFD: High-end residential and office developments. Other emerging zones include Kairouan and Agate, which are well-connected via highways and business parks. Malaz offers stable, centrally located rentals.

Strategic Takeaways for Investors:

Capitalise on transformation by investing in areas tied to infrastructure or mega-projects (Metro, New Murabba, Park, KAFD) to harness growth and appreciation.

Prioritise locations with solid rental demand and institutional interest (e.g., family neighbourhoods, business zones).

Understand local dynamics: Use regulated, licensed developers; be mindful of community fees, handover timelines, and transparency.

Consider foreign ownership structures: Take advantage of new freehold ownership rules and residency incentives.

Factor in policy and taxes: The white land tax may impact undeveloped land; monitor for future regulatory shifts.

DAR Global:

The leading developer in Saudi Arabia with an international presence is the London Stock Exchange-listed DAR Global.

Having launched 200 ultra-exclusive villas in partnership with Mouawad, along with a Trump tower in Jeddah, 2025 has been about acquisitions and the planning for future launches in Riyadh. We are expecting a Trump Tower in Riyadh by 2026, along with a multi-layered master plan featuring luxury Villas, Apartments, and a Trump International Golf Club on an unspecified, expensive plot.

Here’s what Dar Global currently has in the pipeline for Riyadh real estate, based on the most up-to-date information:

SAR 880 Million (≈ $235M) Luxury Residential Project with MouawadDar Global has partnered with luxury jeweller Mouawad to deliver a highly branded residential project near the World Expo 2030 site in north Riyadh. The development comprises 200 luxury villas, merging contemporary design with Mouawad’s craftsmanship—positioned to become one of Riyadh’s most prestigious addresses.

Key strategic advantages:

Taps into Saudi Arabia’s Premium Residency program, where buyers investing SAR 4 million (≈ $1 million) or more are eligible for residency benefits. Represents Dar Global’s market entry into Saudi Arabia, introducing internationally branded luxury residential standards.

Land Acquisitions in Riyadh — $297 MillionIn March 2025, Dar Global invested $297 million to acquire 190 fully developed plots in Riyadh from its parent company, Dar Al Arkan. These plots are projected to yield a gross development value (GDV) of around $800 million.

Why it matters:

This significant land purchase positions Dar Global to launch additional residential-led developments in Riyadh, expanding beyond the Mouawad villas into broader luxury or high-end residential offerings. DAR Global is famous for its branded residences with Lamborghini, Pagani, Trump, Fendi, W, Missoni, Elie Saab, Mouawad and others among its elaborate list of branded options across the globe. Expect some of the most prominent designers and brands to enter the Saudi market in 2026 and beyond.

Strategic Context & Outlook

Dar Global is establishing a strategic footprint in Saudi Arabia, leveraging its parent Dar Al Arkan’s local expertise and relationships.

The company is pursuing a brand-driven approach, partnering with luxury names like Mouawad to differentiate its properties and appeal to wealthy, internationally mobile clients.

Combined with the land investments, Dar Global appears poised to become a leading luxury developer in Riyadh, aligning with Vision 2030’s broader goals of economic diversification and global appeal.

Final Thoughts:

Riyadh is currently one of the most dynamic and opportunity-rich real estate markets in the region, driven by infrastructure, broad reforms, and rapid economic diversification. With high yields, robust capital appreciation, and more open access for international investors, it’s a compelling time to consider strategic real estate ventures.

That said, success hinges on due diligence, selecting the correct location, understanding regulatory frameworks, and aligning with long-term secular trends rather than speculative fever.

Let me know if you’d like help diving into specific neighbourhoods, returned yields, developer reputations, or navigating foreign investment compliance.

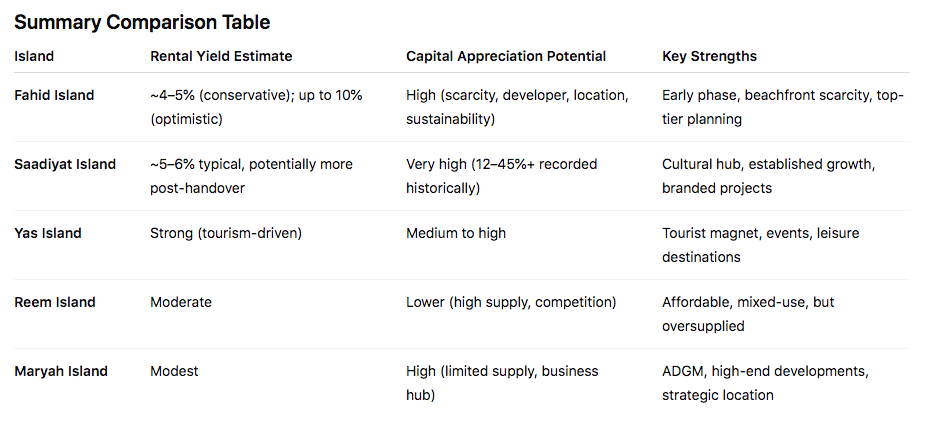

Fahid Island – The real estate jewel in Abu Dhabi’s crown

With the upcoming launch of Fahid Beach Terraces in Abu Dhabi. Like ourselves, many of you are seeing the potential. As always, we like to provide you with as much information as possible to make informed decisions based on trends, previous numbers and potential forecasted pitfalls.

Fahid Island Investment Overview Here’s a clear and investor-focused overview of Fahid Island in Abu Dhabi, detailing expectations for rental yields, capital appreciation, and how it compares to other local island developments.

Rental Yields Early projections suggest annual gross rental yields of 4–5% for 1–3 bedroom apartments (based on today’s prices). Some marketing sources cite yields as high as 7–10%, although these predictions may be overly optimistic.

Capital Appreciation Potential Fahid Island has strong long-term growth potential due to several factors:

– There is a limited supply of beachfront units and villas. Its strategic location between Saadiyat and Yas Islands, near major attractions and infrastructure. – Development by Aldar, a reputable and financially stable developer. – Sustainability certifications such as Fitwel, LEED Platinum, and Estidama 3 Pearl enhance the appeal for tenants and investors.

Comparable areas have exhibited robust appreciation:

Saadiyat Island

– On Saadiyat Island, luxury villas have appreciated by over 45% from 2021 to the current day. – Reports indicate that all properties on Saadiyat have increased in value by 45% over the past three years. -One investment project account noted a 171% price increase for 2–3 bedroom apartments on Saadiyat since 2022.

Yas Island

Apartments (1 Bedroom):

Average sale price has risen significantly from AED 836,000 in 2020 to about AED 1,290,000 in 2025, an increase of approximately 54%.

Villas:

– 4-bedroom villas appreciated from around AED 4.3 million in 2020 to AED 5.6 million in 2025, reflecting a 30% increase.Larger – 5- to 6-bedroom villas experienced even more substantial gains, with increases ranging between 33–61% over the same period.

Recent Year-on-Year Trends (2024–2025):

– Overall premium property segments in Abu Dhabi, including Yas Island, saw average price growth of around 5.3% in Q2 2025. – For luxury apartments on Yas Island, the annual return (ROI) stands at approximately 6.99%, with average sale prices at AED 1.87 million. – Luxury villas are averaging AED 4.68 million, delivering a 5.53% ROI. – In 2024, Yas Island saw a per-square-foot price increase of roughly 11.3%, marking it as one of the fastest-growing areas in Abu Dhabi.

Early-Mover Advantage:

As Fahid Island is in its initial launch phase, it offers lower entry prices with significant upside potential as infrastructure and demand grow. Aldar promptly launched a second residential tower following high demand on the same day. Fahid Beach Terraces is on the waterfront. This is where you see the most premium options with the most significant potential.

Comparison with Other Abu Dhabi Islands

Saadiyat Island: Known as a cultural hub, featuring the Louvre and a planned Guggenheim. It has historically strong appreciation (12–45% in recent years).

Yas Island: A tourism and leisure powerhouse, offering attractions like the F1 Grand Prix and Ferrari World. Investors report excellent short-term rental yields due to high tourist demand.

Reem Island: A mixed-use development with high supply, experiencing some rental spikes, but facing challenges like lower appreciation and oversupply.

Maryah Island: A fast-growing financial district anchored by ADGM, known for its limited supply and high appreciation potential.

Final Thoughts for Investors

Fahid Island presents a compelling value proposition with its limited beachfront real estate, prestigious development by Aldar, eco-conscious design, and early pricing advantages. The conservative rental yield expectation is 4–5%, with potential upside to 7–10% due to strong rental demand. Capital appreciation is anticipated to be robust as the island matures.

Saadiyat Island serves as a benchmark for capital appreciation in Abu Dhabi and remains a smart choice for those seeking long-term value growth in a proven cultural district. Yas Island is ideal for short-term rental strategies, thanks to the influx of tourism and events. Reem Island may appeal to buyers looking for lower entry-level options, but they should expect slower appreciation and higher competition. Meanwhile, Maryah Island offers prestige and a limited supply with robust business demand potential.

Fahid Island for us offers a blend of all of the above. We are fortunate to have witnessed the future development in scale, and anyone who purchases in the initial stages will be sitting on some of the strongest real estate in the UAE.

Dear Investors,

I hope you’re all doing well.

Our advisory and office has recently placed ever-growing emphasis on Abu Dhabi as an investment destination. We have done this for several reasons, but here are the numbers behind our decision to place a substantial interest in the Abu Dhabi Market.

Before we start, this isn’t a slant on Dubai. Dubai is my family home for a good proportion of the year. It’s where Off Plan Dubai is based, and the market is as strong now as we have ever been. However, we must consider reports like the Fitch report as they stand; you cannot simply overlook the potential negatives and focus solely on the positives.

Below is a tight, practical comparison of Abu Dhabi vs Dubai for H2-2025 and into 2026 (the next 18 months), plus a clear recommendation depending on your risk/timeline.

Quick headline summary

Abu Dhabi: steadier, supply-constrained, institutional demand (Aldar, Modon etc..). Expect continued modest price/rental gains and lower volatility.

Dubai: enormous transaction volumes and rapid price gains in 2024–H1- 2025 but facing meaningful downside risk from rising supply – some forecasters (Fitch) expect a correction through H2-2025/into 2026: higher upside potential but higher short-term risk.

Future Property Supply Vs Population Growth

Abu Dhabi purposely launches fewer projects, whereas Dubai has many private developers, resulting in more frequent launches. A typical off-plan project takes 3-4 years to complete. So let’s look at the Population Growth numbers vs the oncoming supply.

2021-2024 Dubai – 212,000 Units sold Abu Dhabi – 22,000 Units sold

Dubai sold just over 9 times more properties than Abu Dhabi in the last 3 years, and that number jumps even further when you look at the sales YTD in both locations.

2025 YTD Dubai – 66,029 Units sold Abu Dhabi – 4,307 Units sold

In Dubai, there’s now a 15-fold increase in the same period for 2025.

Population Growth (June 2025 We received the census for 2024.)

Dubai – 169,000 increase (+4.5% = 3.86 million added) Abu Dhabi – 288,840 increase (+7.5% = 4.14 million added)

As of June 2025, the population of the United Arab Emirates stands at 11.35 million. Both the populations in Abu Dhabi and Dubai are very similar, with each having just under 4 million people. The density in Abu Dhabi is much lower.

Measuring the impact of these numbers?

For every off-plan unit sold, we can see how many new residents were added to fulfil that level of demand.

In Dubai: 1.5 new residents per off-plan unit sold. In contrast; Abu Dhabi: 27 new residents for every off-plan unit sold.

The numbers show that in Abu Dhabi, you can be fully assured with any off-plan purchase that the increase in population will impact the demand, and ultimately the value and rental yield over the coming years. Tight supply, with increased growth, is the bedrock of any thriving real-estate market. This can be seen as a country as a whole, or in micro-markets across the region.

What does that mean for H2-2025 → 2026 (next 18 months)

Expectation: modest-to-solid price and rental growth (single-digit % gains over the next 12–18 months likely), lower downside risk. Suitable for capital preservation + steady yield.

Dubai (higher upside, higher risk)

Why: extremely high transaction velocity and investor appetite, lots of off-plan launches and villa building → possibility of oversupply; macro/credit risks could trigger a correction.

Expectation: higher short-term volatility — pockets (villas/prime) may continue to outperform; some analysts warn of a price correction up to mid-teens % if supply and sentiment shift, best rewards if you buy right (location/timing) and can stomach potential downside.

Conclusion:

In Dubai, be picky, vigilant and invest in the best products in the best locations. Use trusted brands/developers who will deliver the strongest options.

Abu Dhabi has its upside. You can live in Hudayriyat Island in a full Sea View villa with a price per sqft of just AED 1600 per sqft. You can comfortably pay that in Dubai to live 20 minutes into the desert.

We will keep you informed of the best options across both regions, and as always, we would only advise what we personally would invest in.

Personally, I am seeing friends and family moving to Abu Dhabi for logistical reasons, such as traffic and a slower pace, as individuals become families. My next personal purchase will be a Villa on Fahid or Hudayriyat Island, as well as the upcoming Trump Tower launch in the Capital.

At Off Plan Dubai, we pride ourselves on bringing investors the best real estate investments in the world. We show up, take action and provide investors with the best options from the world’s leading developers.

2025 has a new player… Saudi Arabia.

As it lies in the GCC and in many ways is the cultural, religious and investment heart of the Middle East, we ask a question that many investors are now asking: Is Saudi Arabia the new Dubai?

Our take is that Saudi Arabia is not the new Dubai, but it is aiming to become something even bigger and more influential in its unique way.

It is May 2002, and Dubai’s real estate landscape is about to change forever. Dubai overnight issues a decree that allowed non-GCC nationals to buy, sell and lease property in selected developments. The property market changed forever, the floodgates were opened, and international buyers and investors, primarily from Europe, South Asia and the Middle East, flooded the market. Developers like Emaar, Nakheel and Dubai Properties launched mega projects such as The Palm Jumeirah, Dubai Marina, Downtown Dubai (Burj Khalifa), Jumeirah Lakes Towers, etc. Prices surged as demand outstripped supply and Dubai’s skyline was to become unrecognisable as construction boomed. To manage this, we saw the creation of regulatory bodies such as RERA (Real Estate Regulatory Authority) in 2007 and the Dubai Land Department (DLD). These bodies brought transparency, regulation, and investor protection into the market.

Last week, we got the news that many had been waiting for: Saudi Arabia is opening its Real Estate market to foreign investors. Over 1200 HNWI have already purchased real estate and taken advantage of the Premium Residency. Still, now we will see whole regions become Freehold and attract international investment that previously may have looked elsewhere. If you could go back in time to 2002, would there have been a better real estate investment location than Dubai? Based on history, the opening of the real estate sector can provide opportunities for early investors that may never be seen again.

Here’s a breakdown of the comparison and how Saudi Arabia is positioning itself to investors:

🔹 1. Different Goals, Different Scale

Dubai became a global hub through tourism, finance, and luxury real estate. It’s a city-state with a fast, nimble model that thrives on growth and foreign investment in the region.

Saudi Arabia is building entire mega-regions, not just a city — think NEOM, The Line, Diriyah, New Murabba, Red Sea Project, and more. These are multi-trillion-dollar visions backed by state wealth with longer timelines.

Riyadh and Jeddah, under the new government reforms, will open many of their locations up for foreign investments. The two cities already hold world-class infrastructure, but the influx of foreign investment will help to drive growth across multiple sectors, such as health, education and Real Estate.

🔹 2. Vision 2030: A National Overhaul

Saudi Arabia’s Vision 2030 isn’t just about real estate or tourism — it’s about:

Diversifying the economy away from oil

Building entire new industries (tech, entertainment, renewable energy)

Massive investments in infrastructure, giga-projects, and tourism

Encouraging foreign direct investment and private sector growth

Opening the Real Estate market for foreign investment was pivotal to this growth. Minister of Municipal Affairs and Housing and Chairman of the Real Estate General Authority. Al Hogail commended the law, calling it “an extension of the Kingdom’s comprehensive real estate reform agenda. “The updated law aims to increase real estate supply, attract global investors and developers, and further stimulate foreign direct investment (FDI) in the Saudi market.”

🔹 3. Real Estate & Investment

Saudi Arabia is now opening up to freehold ownership for foreigners in key zones — this is a game-changer, much like Dubai’s 2002 freehold reform. 2002 overnight changed the game for Dubai.

Demand is growing for luxury residences, hospitality assets, and commercial hubs, but it’s earlier in the curve than Dubai, which may be suitable for long-term investors.

🔹 4. Tourism & Lifestyle

Dubai is already a leisure powerhouse with global appeal.

Saudi Arabia is catching up fast: launching events (like Riyadh Season), building tourist destinations (like AMAALA, Red Sea), and easing social restrictions (music, cinema, fashion).

🔹 5. Legal & Cultural Factors

Dubai offers a more liberal environment, which attracts many Western expats and tourists.

Saudi Arabia is liberalising, but remains more conservative, though the pace of change has surprised many. Off Plan Dubai spends time regularly in Riyadh and Jeddah, and you will not find anywhere more welcoming and family-oriented.

🔹 Final Take: “Saudi Arabia is not the new Dubai — it’s the new Saudi Arabia.”

Dubai is a city; Saudi Arabia is a nation of 36 million with resources, space, and ambition to reshape the entire Middle East.

If the current momentum continues, Riyadh, NEOM, and Jeddah could rival Dubai, not just as competitors, but as part of a new multi-polar Gulf.

We are firm believers in the full strength of the region. A dynamic, responsive and growing Saudi Arabia is only a positive for the region. HNWI, Family, and private offices looking to establish and open offices in Saudi Arabia will still primarily drive growth and tourism to the UAE.

If you’re thinking from an investment angle, Saudi Arabia may offer:

Higher long-term upside

Early-mover advantage

More risk, but also more reward than the now-mature Dubai market.

Since the middle of 2024, you have seen developers enter the Saudi Market, aligned with some of the most prominent names in the Real Estate world. Trump Tower Jeddah, which is due to be followed by a sister tower in 2026 in Riyadh, as well as the launch of a Trump Masterplan with Golf Course and Villas. DAR Global has launched House of Mouawad Villas in Riyadh, which has been purchased by some of the most prominent business people across the world as the value hits the premium residency requirements for its buyers.

We will always keep investors informed on opportunities across both regions and we are excited to see if the new legislative reforms impact the Saudi market as they did the UAE.

New Murabba has set the Riyadh Investment landscape ablaze with the announcement of the world’s largest downtown area. The scale of the project is awe-inspiring, focusing on the world’s largest structure, the ‘Mukaab’. Off-plan Dubai, at the end of 2023 and throughout 2024/25, has aggressively worked the Saudi market, as we believe it holds some of the world’s most interesting opportunities, with the opening of Premium Residency and the level of wealth entering the region.

Off Plan Dubai will be aligning with New Murabba, a PIF-funded developer, and will provide investors with options for purchasing some of the most exciting Real Estate anywhere in the world. As with any significant new development, it is essential to examine both the Pros and potential Cons.

Here’s a comprehensive look at New Murabba and what it means for Riyadh, including whether residential units are a wise investment in New Murabba.

📌 What is New Murabba?

Scale & scope

Massive 19 km² (≈25 million m² of built area) mixed-use district in northwestern Riyadh, launched Feb 2023 as part of Vision 2030

It will house 104k–119k residential units, 9k hotel rooms, 980k–1.4 M m² office space, ≥500k m² retail, 620k m² leisure, 180–1.8 M m² community facilities, a 45k-seat stadium, university, museum, and 80+ cultural venues

The Mukaab

A central 400 m cube skyscraper — tallest, widest, longest — offering immersive retail, hospitality, residential, cultural, digital experiences, topped with creative tech holographics

Aims to be the world’s largest by volume and a digital‑physical landmark

Smart & sustainable city

Designed as a 15‑minute city with walkable green corridors, cycling, internal transit, smart energy grids, water reuse, waste recycling, and EV charging.

Economic ambition

Projected to add SAR 180 billion (~USD 48 billion) to non‑oil GDP and create 334k jobs by 2030

🌆 Impact on Saudi Arabia & Riyadh Market

Urban tech hub & tourism magnet It solidifies Riyadh’s position as a global destination for culture and innovation, attracting businesses and talent. New Murabba aim to build the most diverse and forward-thinking Downtown anywhere in the world.

Infrastructure catalyst With Metro and metro‑adjacent transport links, internal public transit, and proximity to the airport, this zone will redefine connectivity.

Real-estate ripple effect

Residential prices in Riyadh average SAR 5,500/m² (£1,050/m²); units inside New Murabba are expected to fetch SAR 8,500/m² (~£1,630/m²)

Commercial and retail spaces are also expected to command premium pricing, benefiting from increased visitor and tenant demand.

Foreign investment & stability

Full foreign ownership rules in Saudi developments, along with the Riyadh riyal’s peg to the USD, provide predictability.

Partnerships with global firms (e.g., Bechtel, Turner Arabia) underpin confidence.

🏠 Is Residential a Good Investment?

Pros

High-quality infrastructure: innovative technology, sustainability, community amenities, educational, and health facilities.

Rising prices: built-in premium with clear upside if demand mirrors global mixed-use developments.

Early-bird advantage: Buying pre-construction or during the early phase is likely to yield better returns.

Regulatory openness: regulator-friendly for international investors.

Cons

Megaproject risks: ambitious timelines can slip; New Murabba targets 2030 finish.

Construction intensity: current chatter suggests that build quality is high, but surrounding construction noise and congestion are expected to persist for a while.

Pricing sensitivity: Will premium pricing be sustained? Riyadh’s broader market must absorb high‑end products.

🎯 Final Take — Strategic Investment?

Long-term residential: yes — particularly for luxury apartments or family condos with high finishes and tech features.

Buy‑to‑let: promising if rental demand arrives from professionals working in the district and short‑term stays.

Speculative flip: Riskier pricing may plateau if rollout delays or broader market softens.

Bottom line: New Murabba is a visionary development that boosts Riyadh’s real estate trajectory. For well-capitalised investors targeting high-end residential, especially those entering early, it presents a strong opportunity — but do your due diligence on construction updates and phasing.

Transport links — completion dates for metro/rail lines influencing connectivity premium.

Market velocity — rental and sales absorption rates in nearby early‑phase units (some real-time rental → ~SAR 50k/year for 3 BHK in newer Murabba areas)

Conclusion As a transformational urban development, New Murabba is poised to reshape Riyadh’s skyline and economy. Residential units here are likely among the best positioned for capital growth, especially for investors who are comfortable with multi-year horizons and potential project volatility.

Please let me know if you’d like insights on specific unit types, pricing trends, or financing options.

Get in touch

Dubai Office

Off Plan Dubai

Suite: 508, Fairmont, Sheikh Zayed Road, P O Box 75671, Dubai, UAE